.png)

Merchant onboarding in the US has become one of the most important strategic functions for payment providers. Every merchant approved creates an opportunity to grow revenue, but also introduces fraud, compliance, operational, and reputational risk. As merchants expect faster activation and regulators demand greater accountability, payment providers are under increasing pressure to balance speed with trusted, defensible decision-making.

The challenge is that merchant onboarding has moved beyond completing verification checks. Verification alone is not merchant onboarding. Verification confirms facts. Trusted onboarding determines whether the overall merchant relationship represents acceptable risk. Business verification, AML screening, underwriting, and other controls remain essential, but they only validate individual pieces of information. The harder question is whether those signals collectively support an acceptable-risk decision.

Leading payment providers are responding by replacing disconnected onboarding processes with end-to-end operating models. By bringing together digital onboarding, product configuration, merchant verification, KYB, KYC, AML screening, underwriting, automated decision-making, ongoing customer due diligence, and workflow management within a single platform, they can activate merchants faster, apply controls more consistently, and scale with greater confidence.

Platforms such as OnBoard by MVSI are designed for this shift, bringing digital onboarding, KYB, AML screening, underwriting, risk decisioning, approvals, and ongoing due diligence into one governed workflow for regulated payments, fintech, and financial services teams.

This guide explores how merchant onboarding in the US is evolving, the challenges of traditional merchant onboarding, and the best practices payment providers can adopt to reduce friction, strengthen decision-making, and support sustainable growth.

Key Takeaways

- Merchant onboarding in the US is becoming a strategic operating function that helps payment providers balance merchant growth, operational efficiency, risk management, and regulatory compliance.

- Modern merchant onboarding connects digital onboarding, merchant verification, KYB, KYC, AML screening, merchant underwriting, and AI-assisted decisioning into a single, end-to-end workflow.

- Structured data, intelligent automation, and management-by-exception workflows help payment providers make faster, more consistent onboarding decisions while reducing unnecessary manual effort.

- Flexible onboarding platforms enable payment providers to support multiple merchant types, jurisdictions, products, partner channels, and brands without sacrificing governance or operational control.

- Extending merchant onboarding into ongoing customer due diligence (OCDD) helps organizations continuously monitor merchant risk and maintain more informed decisions throughout the customer lifecycle.

What is merchant onboarding in the US?

Merchant onboarding in the US is the process payment providers use to evaluate, approve, and activate businesses so they can begin accepting electronic payments. It brings together digital onboarding, merchant verification, Know Your Business (KYB), Know Your Customer (KYC), Anti-Money Laundering (AML) screening, merchant underwriting, and risk assessment to determine whether a merchant aligns with the provider's risk appetite, compliance obligations, and commercial objectives.

Merchant onboarding is more than collecting information and completing verification checks. It is a strategic function that enables payment providers to make informed, consistent, and scalable onboarding decisions while balancing merchant growth, operational efficiency, risk management, and regulatory compliance.

As fraud becomes more sophisticated, business models evolve, and scrutiny increases, delivering a fast, connected, and well-governed merchant onboarding process is becoming increasingly important.

In that sense, merchant onboarding is not just a verification process. It is the operating model that turns business, owner, compliance, underwriting, and risk signals into a trusted onboarding decision.

How US regulations are reshaping merchant onboarding

Recent regulatory developments are raising the standard for merchant onboarding in the United States. Payment providers are under increasing pressure to make faster onboarding decisions while demonstrating stronger governance, greater consistency, and clearer evidence of how merchant risk is assessed.

For banks, covered financial institutions, and payment providers operating through regulated banking or acquiring relationships, the Bank Secrecy Act (BSA), and FinCEN's Customer Due Diligence (CDD) Rule, and sanctions compliance expectations help shape how merchant onboarding is designed and governed. These requirements go beyond confirming that a business exists. Payment providers are expected to understand who owns the business, how it operates, the risks it presents, and continue monitoring those risks throughout the merchant relationship. This raises the importance of structured onboarding and leaves less room for inconsistent decision-making.

OFAC sanctions compliance also plays an important role in US merchant onboarding. For payment providers, sanctions screening should not sit as a disconnected check. It should be part of a governed onboarding workflow that connects merchant data, ownership information, risk indicators, escalation rules, and audit trails.

Recent developments are raising expectations even further. In June 2026, US regulators proposed new Customer Identification Program (CIP) requirements under the GENIUS Act for Permitted Payment Stablecoin Issuers. If adopted, stablecoin issuers would need stronger, risk-based procedures to identify customers, verify identities, maintain records, and manage situations where identities cannot be confirmed. While this proposal is specific to permitted payment stablecoin issuers, it signals a wider direction of travel for payment-related financial services: stronger customer identification, clearer records, risk-based procedures, and more governed onboarding controls.

The growing focus on risk-based onboarding extends beyond the United States. Following the FATF June 2026 Plenary, Bosnia and Herzegovina and Iraq were added to the list of jurisdictions under increased monitoring. These changes should be considered in jurisdiction risk analysis, onboarding risk ratings, and escalation workflows where relevant. FATF does not call for enhanced due diligence measures for jurisdictions under increased monitoring, but it does encourage a risk-based approach that takes this information into account.

Taken together, these developments are reshaping what modern merchant onboarding needs to deliver. Isolated verification checks, manual reviews, and disconnected point solutions are becoming harder to defend as scrutiny increases. Payment providers need connected onboarding processes that can consistently collect, verify, assess, and govern merchant risk, while supporting faster, more confident onboarding decisions.

Why traditional merchant onboarding is no longer enough

The regulatory landscape is not becoming simpler, and neither are the expectations placed on merchant onboarding. Payment providers that continue to rely on traditional onboarding processes will face growing pressure to demonstrate consistent decision-making, stronger governance, and greater operational control. As those expectations sharpen, five operational challenges are becoming increasingly difficult for payment providers to overcome.

Lack of support for risk-based decisions

Modern regulations increasingly expect payment providers to apply different levels of scrutiny based on the level of risk each merchant presents. As business models, ownership structures, jurisdictions, products or services, and transaction profiles become more diverse, onboarding needs to adapt accordingly.

Traditional onboarding models were never designed for this level of flexibility. Many payment providers still rely on physical documents, email chains, spreadsheets, or multiple standalone solutions that make it difficult to apply different onboarding journeys based on risk. Instead of focusing attention where it matters most, teams are often forced into manual reviews that create unnecessary friction for lower-risk merchants while making higher-risk relationships harder to assess consistently.

Verification without context creates blind spots

Passing KYB, KYC, or AML checks does not automatically mean a merchant should be onboarded. Each verification provides valuable information, but no single check provides enough context to determine the merchant's overall risk.

As scrutiny increases, payment providers need to know they are making a defensible onboarding decision, not just completing the right checks. When ownership, business activity, transaction behavior, underwriting, and jurisdiction risk are reviewed separately, critical warning signs can be missed. The result is more uncertainty, more manual reviews, and weaker confidence that each decision will stand up to review.

One-size-fits-all onboarding creates unnecessary friction

As merchant onboarding comes under greater regulatory scrutiny, some payment providers respond by requesting more documents, more evidence, and more manual reviews. Rather than making onboarding more intelligent, additional compliance requirements are often passed on to every customer.

Legitimate merchants are often asked to complete unnecessary checks, provide the same information multiple times, or wait for manual reviews that add little value. The result is more friction, slower activation, and higher abandonment at a time when merchants expect fast, seamless onboarding experiences.

Manual processes don't scale with growth

Traditional onboarding may work at lower merchant volumes, but the cracks quickly begin to appear as application numbers grow. Manual reviews, repeated document requests, and disconnected workflows create growing pressure on compliance, underwriting, and operations teams.

Instead of becoming more efficient, onboarding becomes more difficult to manage consistently. Processing times increase, operational costs rise, and maintaining the consistency expected by regulators become increasingly difficult without adding more people or more review stages.

Weak governance creates greater regulatory exposure

Today's regulatory environment expects payment providers to demonstrate not only what decision was made, but how and why it was made. Every onboarding decision needs to be consistent, traceable, and supported by a clear audit trail.

When information is spread across emails, physical documents, and disconnected systems, maintaining that level of governance becomes increasingly difficult. As obligations become more complex, inconsistent decision-making and incomplete audit trails become harder to defend, exposing payment providers to greater operational and regulatory risk.

The expectations have changed, but many onboarding processes have not. As payment providers face greater regulatory scrutiny and growing merchant volumes, relying on traditional onboarding models becomes increasingly difficult to justify. Modern merchant onboarding solutions are making it possible to overcome these challenges through connected workflows, intelligent automation, and risk-based decision-making that improve both operational efficiency and governance.

What modern merchant onboarding should look like

The challenges facing traditional merchant onboarding are not being solved by adding more verification checks or introducing more manual reviews. Modern payment teams are rethinking how merchant onboarding is designed, replacing fragmented processes with connected workflows that improve decision-making, reduce friction, and strengthen governance.

Modern merchant onboarding is not defined by a single capability. It is the combination of connected data, intelligent automation, configurable workflows, and continuous risk management that enables payment providers to onboard merchants faster while maintaining confidence in every decision.

Capture structured data from the start

Every onboarding decision starts with the information collected from the merchant. Modern onboarding replaces static, one-size-fits-all forms with dynamic onboarding forms that adapt based on merchant type, products or services, jurisdiction, partner channel, and risk.

This creates a consistent foundation for merchant verification, underwriting, and risk assessment while reducing unnecessary data collection and improving data quality across the onboarding journey.

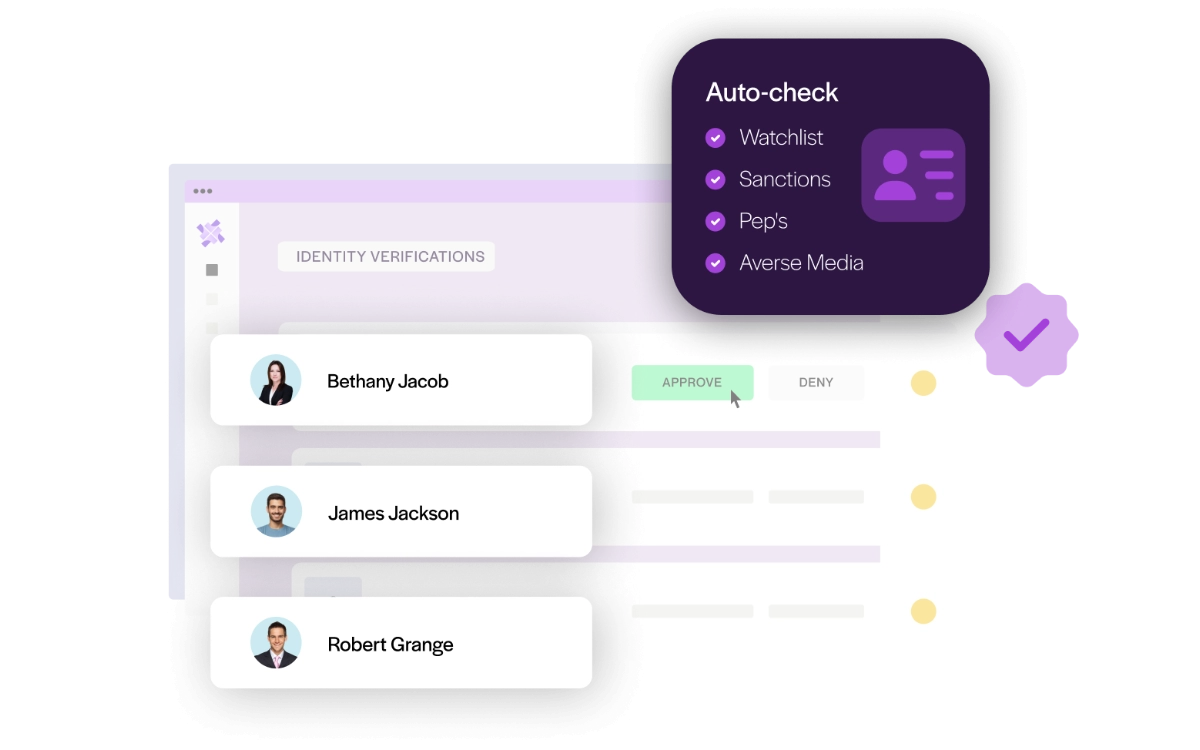

Bring KYB, KYC, AML, and underwriting into one workflow

Once structured merchant data has been captured, it should drive every stage of the onboarding journey. Rather than sending applications between separate systems for KYB, KYC, AML screening, PEP and sanctions screening, merchant underwriting, and risk assessment, well-governed payment providers connect these activities within a single workflow.

This creates a single source of truth for every application, allowing onboarding teams to assess merchant risk holistically instead of relying on isolated verification results. The outcome is faster decisions, greater consistency, and a stronger foundation for trusted merchant onboarding.

Connect real-time data with AI-assisted decisioning

Modern onboarding platforms use real-time data processing, API integrations, configurable business rules, and AI-assisted decisioning to enrich merchant information as applications progress. Rather than replacing human judgment, AI helps organize, validate, and analyze information faster so teams can make better-informed decisions.

By reducing manual validation and presenting risk in context, payment providers can improve consistency, shorten onboarding times, and maintain consistency as application volumes continue to grow.

Automate onboarding through management by exception

Once merchant data is structured, compliance checks are connected, and AI-assisted decisioning is applied, payment providers can automate routine onboarding steps with greater confidence and control. Information flows seamlessly between each stage of the onboarding journey, allowing risk to be assessed continuously and in real time rather than through disconnected reviews.

This enables a management-by-exception approach, where lower-risk merchants can progress automatically while higher-risk or incomplete applications are intelligently escalated for manual assessment. Compliance and risk teams can focus on the applications that require expert judgment, while legitimate merchants benefit from a faster, more consistent onboarding experience.

Build governance into every onboarding decision

Every input, data change, verification result, risk assessment, underwriting decision, escalation, reviewer action, approval, and exception should be automatically captured as the merchant progresses through onboarding. Rather than relying on manual notes or separate records, every action is documented in real time within a single onboarding record.

This creates a complete, traceable record of every onboarding decision, making it easier to identify gaps, minimize blind spots, and understand exactly how each decision was reached. With every action fully traceable, payment providers can reduce regulatory exposure, strengthen governance, and demonstrate a clear, defensible audit trail whenever decisions are reviewed.

Support growth with flexible, multi-jurisdiction onboarding

Growth often means expanding across new markets, products, brands, and partner channels. Flexible onboarding workflows allow payment providers to adapt onboarding journeys, branding, compliance requirements, approval rules, and risk models without creating unnecessary operational complexity.

The same flexibility also supports partner-led growth through white-label merchant onboarding. ISOs, agents, resellers, and regional partners can deliver a trusted, branded merchant experience, while payment providers maintain centralized governance over onboarding workflows, compliance controls, risk rules, approvals, OCDD, and reporting. This enables organizations to expand across partner networks and multiple jurisdictions without sacrificing consistency, visibility, or control.

Extend onboarding into ongoing customer due diligence

Once a merchant is live, onboarding should not stop. Merchant risk continues to change as ownership, transaction behavior, business activities, or sanctions and PEP status evolve over time.

By extending onboarding into ongoing customer due diligence (OCDD), payment providers can continuously monitor these changes, respond faster to emerging risks, and maintain an up-to-date view of merchant risk throughout the entire relationship.

Checklist: Is your merchant onboarding built for the future?

Use this checklist to evaluate whether your merchant onboarding solution supports the capabilities needed for modern, risk-based onboarding.

- Captures structured merchant data through dynamic smart forms that adapt to business type, jurisdiction, partner channel, and risk profile.

- Unifies KYB, KYC, AML, PEP and sanctions screening, and underwriting into a single onboarding workflow.

- Uses AI-assisted onboarding to enrich data, validate information, and support real-time decision-making.

- Supports management by exception by automatically progressing lower-risk merchants and escalating higher-risk applications.

- Creates fully traceable onboarding records by documenting every input, verification, decision, reviewer action, approval, and escalation in real time.

- Supports configurable workflows across jurisdictions, merchant types, products, brands, and partner networks.

- Extends onboarding into ongoing customer due diligence (OCDD) through continuous merchant monitoring and ongoing risk assessment.

- Supports white label and partner-led onboarding across ISOs, agents, resellers, brands, and regions while keeping compliance, risk, approvals, OCDD, workflows, and reporting centrally governed.

Modern merchant onboarding is about making better decisions

Merchant onboarding in the United States has evolved beyond a compliance process. As scrutiny increases and merchant expectations accelerate, payment providers need to make faster, more consistent, and more defensible onboarding decisions without compromising the merchant experience.

Meeting those expectations requires more than adding verification checks or introducing additional manual reviews. It requires a connected onboarding model that brings together structured data, merchant verification, KYB, KYC, AML screening, PEP and sanctions screening, underwriting, AI-assisted decisioning, automation, governance, and ongoing customer due diligence into a single workflow.

This is what OnBoard by MVSI is built for: helping regulated teams move beyond isolated verification checks toward trusted, auditable onboarding decisions. As an end-to-end merchant onboarding and compliance platform for regulated payments, fintech, and financial services, OnBoard by MVSI brings together digital onboarding, KYB, KYC, AML screening, underwriting, approvals, and ongoing customer due diligence (OCDD) within one controlled workflow.

By replacing fragmented processes with a connected merchant onboarding platform, payment providers can improve operational efficiency, strengthen governance, make more trusted, auditable onboarding decisions, and build scalable onboarding models that support long-term growth.

Disclaimer: This article is provided for informational purposes only and does not constitute legal, regulatory, or compliance advice. Merchant onboarding requirements, AML obligations, and customer due diligence expectations vary across jurisdictions and business models. Organizations should seek appropriate professional advice when designing or reviewing their onboarding processes.

Related Merchant Onboarding Resources

Learn how OnBoard helps US payment providers, PayFacs, ISOs, lenders, banks, and regulated businesses accelerate merchant onboarding while strengthening KYB, AML screening, underwriting, governance, and ongoing due diligence.

Merchant Onboarding: How to Speed It Up With the Right Solution

Explore the biggest causes of onboarding delays and discover practical strategies to accelerate merchant approvals while maintaining strong risk management and compliance controls.

Business Lending Onboarding in the US: Managing Compliance, Risk, and Growth

See how US business lenders streamline customer onboarding, strengthen risk-based decision-making, and improve operational efficiency through connected onboarding and compliance workflows.

Frequently Asked Questions

Can merchant onboarding be fully automated?

Many stages of the merchant onboarding process can be automated, including data collection, verification, screening, and routine decision-making. However, higher-risk or incomplete applications still require human judgment. This is why many payment providers adopt a management-by-exception approach, allowing lower-risk applications to progress automatically while specialists focus on higher-risk cases.

What is the difference between merchant onboarding and ongoing customer due diligence (OCDD)?

Merchant onboarding evaluates and approves a business before it begins accepting payments. Ongoing customer due diligence (OCDD) extends beyond onboarding by continuously monitoring changes in merchant risk, ownership, business activity, and sanctions or PEP exposure throughout the customer relationship.

What should payment providers look for in a merchant onboarding platform?

A modern merchant onboarding platform should combine digital onboarding, merchant verification, KYB, KYC, AML screening, merchant underwriting, AI-assisted decisioning, workflow automation, governance, audit trails, and ongoing customer due diligence within a single connected workflow.

What is the difference between merchant verification and merchant onboarding?

Merchant verification confirms specific facts about a business, owner, document, or data point. Merchant onboarding is broader. It connects verification with KYB, KYC, AML screening, sanctions screening, underwriting, risk assessment, approvals, audit trails, and ongoing customer due diligence to determine whether the merchant represents acceptable risk.

How does AI-assisted onboarding improve merchant onboarding?

AI-assisted onboarding helps payment providers validate merchant information, enrich data, identify potential risks, and support faster decision-making using real-time information. Rather than replacing human judgment, it reduces manual effort, improves consistency, and enables teams to focus on applications that require expert review.

What are the merchant onboarding compliance requirements in the United States?

Merchant onboarding in the United States is primarily governed by the Bank Secrecy Act (BSA) and FinCEN's Customer Due Diligence (CDD) Rule. Payment providers are expected to verify merchant identities, understand beneficial ownership, assess merchant risk, perform appropriate AML screening, and maintain ongoing customer due diligence throughout the merchant relationship. Together, these controls support more informed, risk-based onboarding decisions.