.png)

Merchant onboarding has become increasingly complex as acquirers and PSPs expand into new markets, products, and partner ecosystems. While verification remains an important part of the process, providers must also evaluate merchant risk, underwriting, and long-term suitability to make consistent onboarding decisions at scale.

For years, the payments industry has operated under the assumption that verification was the answer to merchant onboarding's biggest challenges.

If identities could be verified, documents validated, and compliance checks automated, onboarding would become faster, smoother, and easier to scale. This belief has driven significant investment in point solutions for Know Your Customer (KYC), Know Your Business (KYB) checks, Anti-Money Laundering (AML) screening, and customer due diligence.

Yet many acquirers and payment service providers (PSPs) still find themselves asking the same questions.

Why is onboarding still taking so long? Why are merchants being asked for the same information multiple times? Why do teams struggle to make consistent decisions? And why does scaling into new markets often create more complexity instead of less?

The reality is that verification alone does not create confidence.

Verification confirms whether information is accurate. Trusted onboarding helps providers decide whether a merchant should be approved, under what conditions, and how that risk should be monitored over time. It brings KYB, KYC, AML screening, underwriting, risk scoring, approvals, auditability, and ongoing due diligence into one consistent decision-making process.

As payment providers expand into new markets, launch new products, and grow through partner ecosystems, that distinction becomes increasingly important. In this article, we'll explore why verified merchants aren't always trusted merchants, why growth demands more than verification, and what providers should look for in an onboarding platform that can support both scale and control.

This is the model OnBoard by MVSI is built to support: an end-to-end merchant onboarding and compliance platform that combines digital onboarding, KYB, AML screening, underwriting, risk workflows, and ongoing customer due diligence in one centrally governed system.

Key Takeaways

- Verification alone does not give providers a complete view of merchant onboarding risk. Providers also need underwriting, compliance, risk, and portfolio context before making confident onboarding decisions.

- Effective merchant onboarding combines KYB, KYC, AML screening, customer due diligence, risk assessment, and underwriting into a single decision-making process.

- Merchant onboarding risk extends beyond compliance and includes credit risk, operational risk, reputational risk, and portfolio fit.

- As providers expand into new markets, products, and partner ecosystems, maintaining consistent onboarding decisions becomes increasingly complex.

- The best onboarding platforms do more than automate checks. They help providers build a complete merchant risk profile and scale growth without losing visibility or control.

The problem with a verification-first mindset

It's easy to see how the industry got here.

Verification was long seen as the biggest obstacle to onboarding. Manual reviews slowed approvals. Compliance checks created bottlenecks. Merchants waited days or even weeks for decisions.

So, the industry did what it does best: it invested in technology.

KYC checks became automated. KYB verification became faster. AML screening became more efficient. Each improvement solved a real problem and helped reduce manual effort.

The challenge is that onboarding was never just a verification problem.

Verifying information is important, but onboarding decisions require much more than confirming whether a business exists or whether documents are valid. Providers still need to understand risk, assess suitability, and determine whether a merchant is the right fit for their portfolio.

As more point solutions were introduced, onboarding often became a collection of separate checks managed by different teams and systems. Compliance reviews one part of the application. Risk reviews another. Underwriting looks at something else.

The result is a process that can successfully verify information while still making it difficult to reach a confident onboarding decision.

And that's where the difference between verification and trust begins.

Why verified merchants aren't always trusted merchants

The problem isn't that verification isn't working. The problem is that verification and trust are not the same thing.

A merchant may pass KYC checks, complete KYB verification, complete AML screening, and provide every required document. Those checks help confirm that the information provided is accurate and complete.

But that merchant may still present elevated risk if its website activity, sales model, ownership structure, product category, refund profile, or operating model falls outside the provider’s risk appetite.

That is why onboarding decisions are rarely based on verification alone.

Providers still need to understand the bigger picture. Does the merchant align with our risk appetite? Is the business model a good fit for the portfolio? Are there credit, operational, or reputational risks that need to be considered? Can the organization confidently stand behind the decision if it is later questioned during an audit or review?

This is where many onboarding processes begin to struggle.

The challenge isn't gathering information. It's bringing together the people, systems, and insights needed to make a confident decision.

Research from Datos Insights found that risk and customer due diligence are often spread across multiple systems, making it difficult for teams to assess merchant risk efficiently. Mastercard also found that many traditional acquirers still rely on back-and-forth emails, phone calls, and manual validation throughout the onboarding process. Together, these findings highlight why many financial institutions are looking for orchestrated solutions that provide a single view of merchant risk and support more confident onboarding decisions.

A verified merchant may satisfy specific identity, business, and AML checks. A trusted merchant is one the organization can approve with a clear rationale, appropriate controls, ongoing monitoring, and an auditable decision record.

Why growth demands more than verification

The distinction between a verified merchant and a trusted merchant becomes far more important as organizations grow.

A payment provider may be able to manage onboarding decisions through experience, manual reviews, and close collaboration when operating within a single market. But that becomes much harder as the business expands.

Many PSPs and acquirers are increasingly relying on partner ecosystems to accelerate growth and gain access to markets they may not have been able to enter on their own. As explored in our recent mini webinar on the strategic advantages of partner-led growth, these partnerships can provide valuable local expertise, established relationships, and a faster path into new markets.

Growth, however, introduces new layers of complexity. Different markets have different regulations, business structures, risk profiles, and onboarding requirements. As more markets, products, and partners become involved, keeping onboarding decisions consistent and aligned with the organization’s risk appetite becomes harder.

Providers are no longer evaluating merchants based solely on compliance requirements. They must also consider merchant credit risk, operational risk, reputational risk, portfolio fit, and long-term viability across every onboarding decision.

This is why trusted onboarding has become a foundation for growth. It provides a consistent way to evaluate merchants, apply controls, and make confident decisions regardless of where a merchant operates, which market they serve, or how they entered the ecosystem.

The foundation of trusted merchant onboarding

A trusted onboarding framework is not about adding more checks. It's about creating a process that helps providers make confident onboarding decisions while maintaining speed, consistency, and control.

When evaluating a merchant onboarding platform, look for these capabilities that support trusted onboarding at scale:

1. A single view of merchant risk

Trust is difficult to build when information is scattered across different systems, teams, and workflows.

A stronger onboarding platform brings the entire merchant journey into a single process, from application, offers, and verification through risk assessment, approvals, and go-live. This creates a complete view of the merchant and reduces the

need for teams to manually connect information across departments.

2. Intelligent workflows that adapt to risk

Not every merchant should follow the same onboarding path.

A trusted onboarding platform should be able to automatically adjust workflows based on merchant type, risk profile, geography, products, and services. Where policy allows, lower-risk merchants can move through onboarding faster, while higher-risk applications are escalated for human review and documented approval.

This helps providers reduce friction without compromising control.

3. Automated decision support, not just automated checks

KYB, KYC, AML, and customer due diligence checks are important, but trusted onboarding requires more than verification.

Look for platforms that combine risk scoring, underwriting, data enrichment, automated risk assessment, and website intelligence. The goal is not only to verify information but also to help teams make more informed onboarding decisions.

For example, website analysis can help validate whether a merchant's declared business model matches their actual online presence, uncover hidden redirects, identify suspicious website behavior, and flag potential scheme-related risks before they become compliance or portfolio issues. These insights provide additional context that helps providers assess merchant risk more accurately and consistently.

4. The ability to scale across markets and partner ecosystems

Growth introduces new regulations, onboarding requirements, and risk considerations.

A trusted onboarding platform should help providers apply consistent controls across different markets, products, and partner channels while maintaining visibility and auditability. This becomes increasingly important as organizations expand into new regions and rely on partners to accelerate growth.

The best onboarding platforms don't just automate onboarding tasks. They create a trusted framework for making consistent decisions at scale.

These principles define what trusted onboarding should achieve. Turning them into a consistent and scalable process requires capabilities that connect onboarding, verification, risk assessment, underwriting, and ongoing due diligence into a single framework.

Capabilities that enable trusted merchant onboarding

The capabilities above define what trusted onboarding looks like in practice. But making it work consistently across merchants, markets, products, and partner channels requires the right tools.

The following capabilities help turn trusted onboarding from a concept into an operational reality.

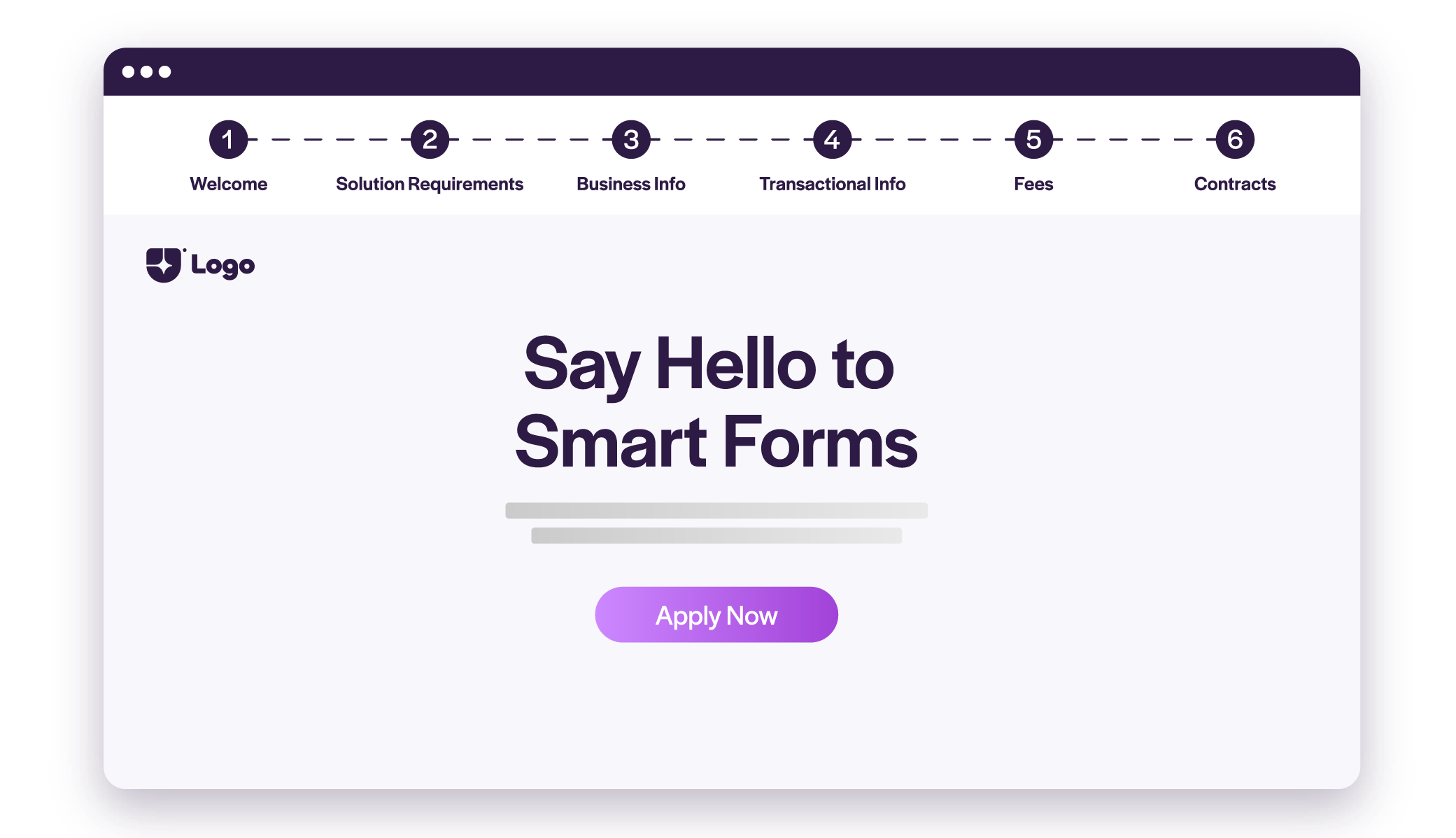

1. Smart Forms

The onboarding journey starts with understanding the merchant. Dynamic smart forms adapt automatically based on merchant type, geography, products, services, legal structure, and risk profile. By collecting the right information at the right time, providers can build a more complete picture of the merchant from the outset, creating the foundation for more accurate risk assessment, underwriting, and onboarding decisions.

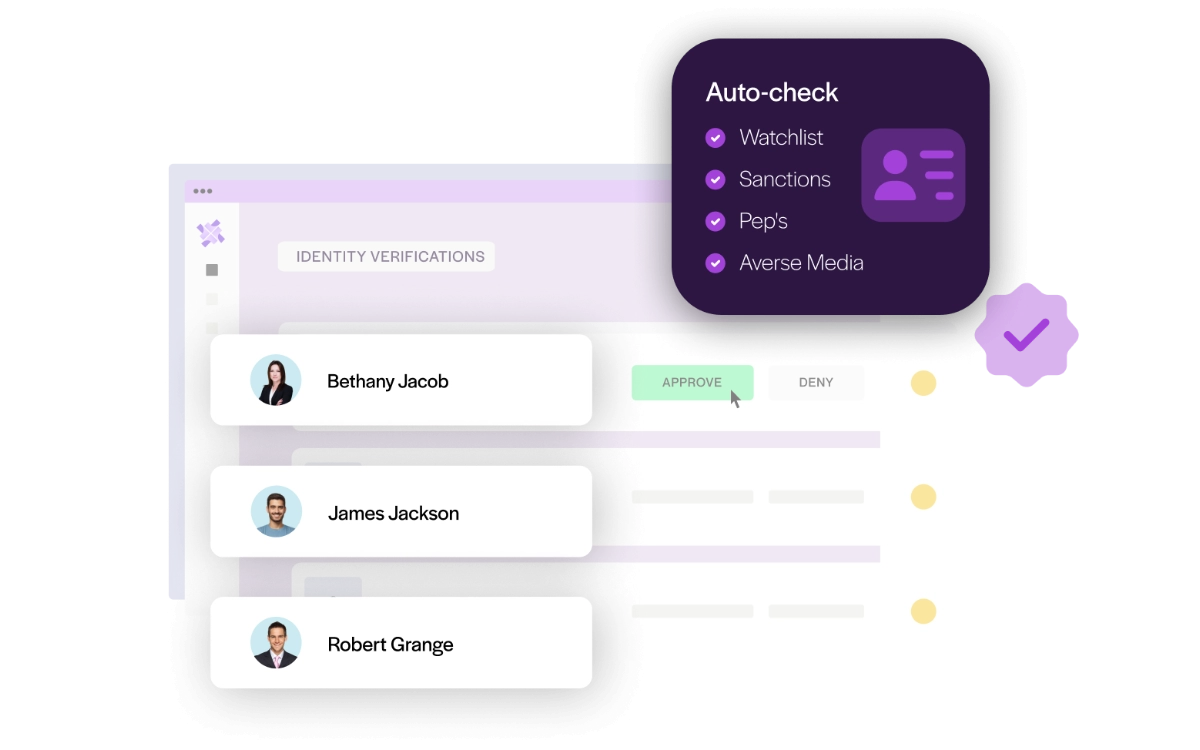

2. Unified KYB, KYC, and AML Verification Workflows

Verification remains a critical part of onboarding, but it should not operate in isolation. KYB, KYC, AML screening, PEP screening, and sanctions screening should be embedded directly within the end-to-end onboarding journey, alongside risk assessment, underwriting, approvals, and fulfillment. This gives teams greater visibility into the full merchant profile and ensures verification results contribute directly to onboarding decisions rather than sitting in separate systems or workflows.

PEP, watchlist, and adverse media checks.

3. AI-Powered Document Intelligence and Website Risk Analysis

One of the biggest challenges in onboarding is turning large amounts of information into something teams can actually use.

AI-powered onboarding helps by reading onboarding documents, extracting key information, validating data, and automatically triggering the necessary actions and workflows. Instead of manually reviewing every document, teams can focus on understanding the merchant and making better decisions.

The same applies to website reviews. AI-powered website intelligence can identify hidden website behavior, validate business activities, and flag potential card scheme risks that may otherwise go unnoticed. This gives providers a deeper understanding of the merchant before making an onboarding decision.

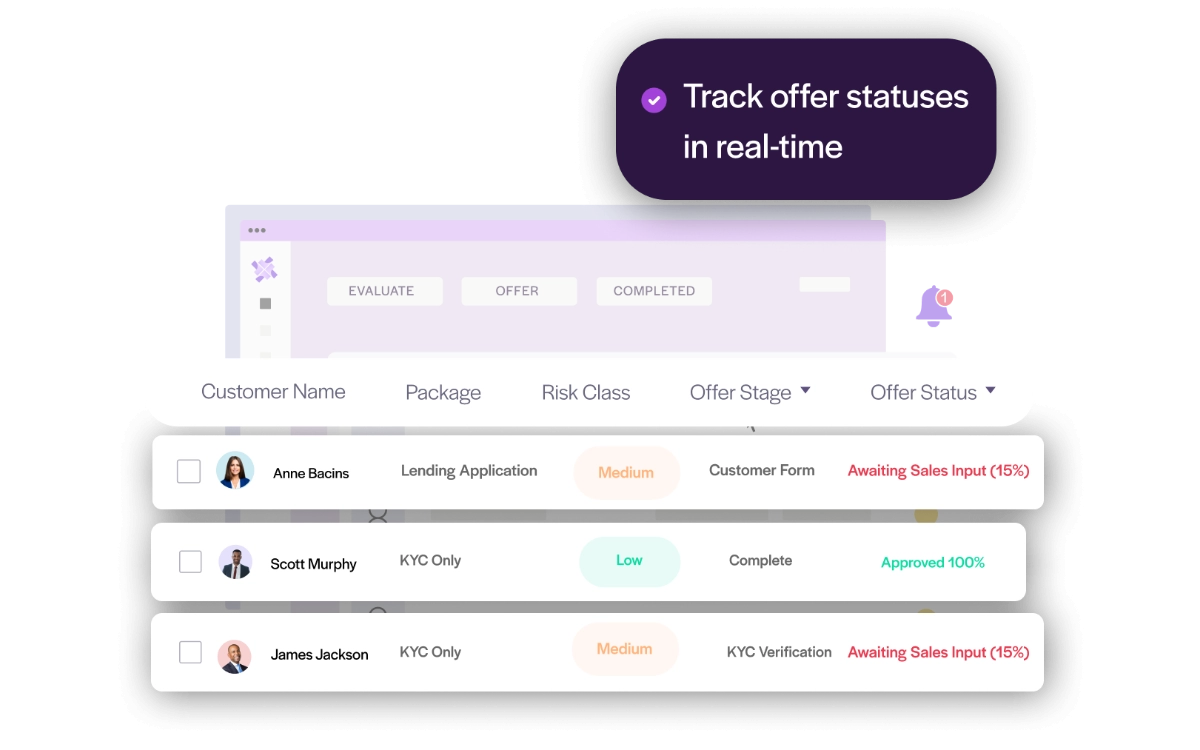

4. Real-Time Risk Scoring and Merchant Underwriting

Real-time risk scoring and merchant underwriting bring together merchant information, verification results, document intelligence, website analysis, customer due diligence, and external data sources into a single merchant risk profile. This creates a centralized merchant risk profile where information can be validated, assessed, and understood in context rather than reviewed as separate checks.

This also enables a management-by-exception approach, where lower-risk merchants can move through onboarding automatically while higher-risk applications are escalated for additional review. This helps teams focus their time on the decisions that require human judgment while maintaining clear escalation paths, decision records, and human oversight where risk, compliance, or underwriting review is required.

risk, offer stages, and onboarding progress.

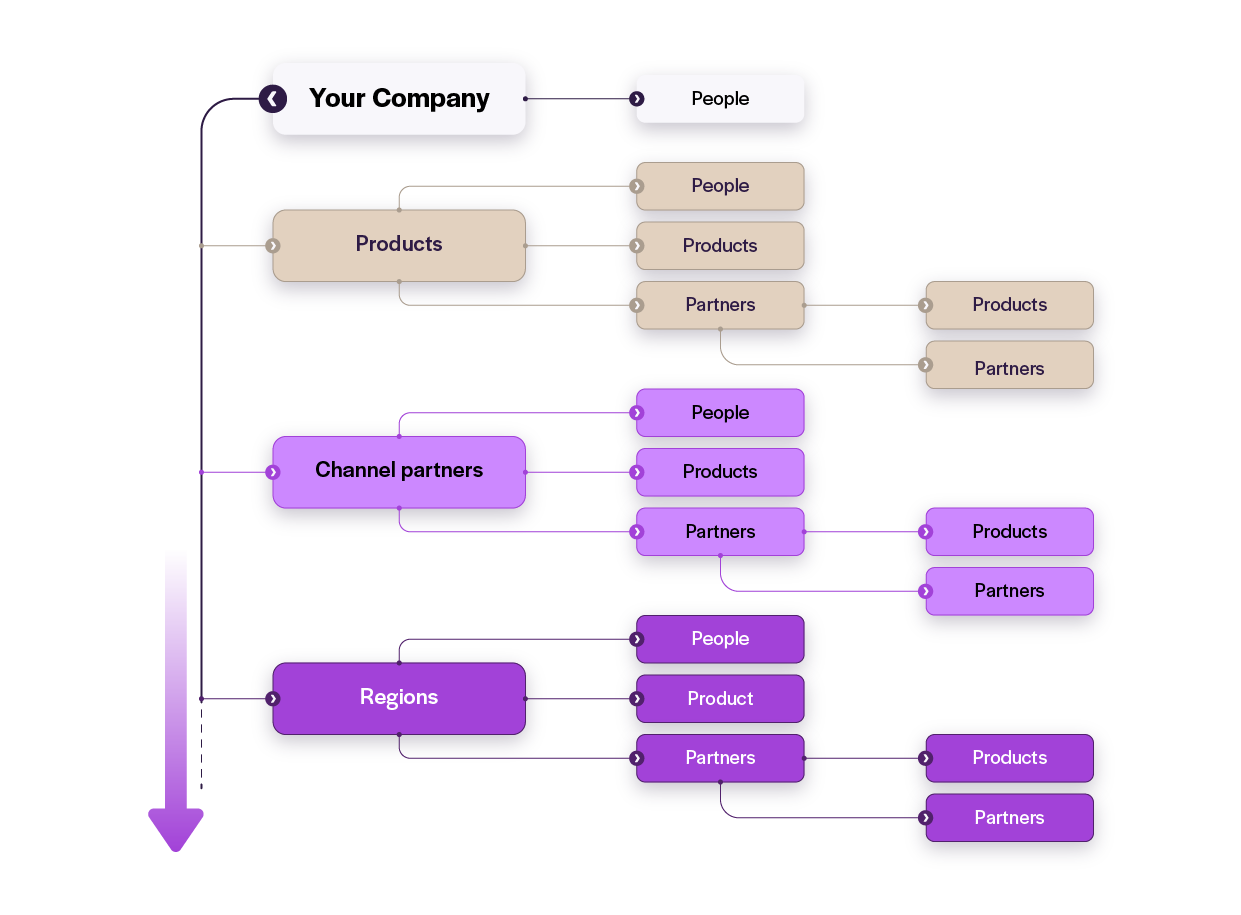

5. Partner-led onboarding with white label control

Partner channels can accelerate growth, but trust becomes harder to maintain when onboarding decisions are distributed across multiple organizations.

White-label onboarding helps providers deliver consistent, branded merchant journeys through ISOs, agents, resellers, and regional partners, while compliance rules, risk scoring, underwriting, approvals, KYB, AML, OCDD, workflows, and reporting remain centrally controlled. This keeps onboarding decisions aligned with the organization’s risk appetite and compliance standards, regardless of which partner introduced the merchant.

journeys across channel partners, products, and regions.

6. Ongoing Monitoring and Ongoing Customer Due Diligence (OCDD)

Trusted onboarding does not end when a merchant is approved.

As businesses evolve, ownership structures change, products expand, and new risks emerge. Ongoing monitoring and ongoing customer due diligence help providers identify these changes early, ensuring onboarding decisions remain valid long after the initial approval.

This allows organizations to maintain confidence in merchant relationships as they grow.

7. Audit Readiness and a Single Source of Truth

Trusted onboarding also depends on being able to explain and defend onboarding decisions.

A single source of truth brings together onboarding data, verification results, risk assessments, approvals, supporting documentation, and decision histories in one place. This gives compliance, risk, and underwriting teams a clear record of how decisions were made and provides the transparency needed for audits, reviews, and regulatory oversight.

As onboarding volumes increase, this becomes critical for maintaining consistency and control at scale.

Conclusion

The payments industry has spent years trying to solve merchant onboarding through better verification.

Verification remains essential, but it is only one part of the decision.

As providers expand into new markets, products, and partner ecosystems, the challenge becomes building enough confidence to onboard the right merchants while maintaining control over risk.

Trusted onboarding helps make that possible.

By bringing together verification, risk assessment, underwriting, and ongoing due diligence into a single process, providers can make more consistent decisions, reduce merchant onboarding risk, and scale growth with confidence.

In the end, the goal is not simply to verify merchants. It is to identify which merchants can be approved with confidence while maintaining appropriate risk controls.

Organizations need onboarding processes that bring together risk assessment, underwriting, compliance, and ongoing due diligence into a single decision-making framework.

OnBoard by MVSI is an end-to-end merchant onboarding and compliance platform for regulated payments, fintech, and financial services, combining digital onboarding, KYB, AML screening, underwriting, and ongoing due diligence (OCDD) in one system. By bringing verification, risk assessment, underwriting, and compliance workflows together into a centralized onboarding framework, organizations can reduce merchant onboarding risk while maintaining visibility, consistency, and control as they scale.

Disclaimer: This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or risk management advice. Regulatory obligations and onboarding requirements vary by jurisdiction, payment ecosystem, and business model. Organizations should consult qualified legal, compliance, risk, and underwriting professionals when designing or updating merchant onboarding programs.

Frequently Asked Questions

What is merchant onboarding risk?

Merchant onboarding risk refers to the potential financial, operational, compliance, reputational, and credit risks associated with approving a merchant. Effective onboarding processes assess these risks before approval to help providers make informed decisions and maintain a healthy merchant portfolio.

Why isn't KYB, KYC, and AML verification enough for merchant onboarding?

Verification helps confirm that information is accurate, but onboarding decisions require more than compliance checks alone. Providers also need to assess merchant onboarding risk, merchant credit risk, business model suitability, and overall portfolio fit before approving a merchant.

What is the difference between a verified merchant and a trusted merchant?

A verified merchant has successfully passed checks such as KYC, KYB verification, AML screening, and customer due diligence. A trusted merchant is one that the provider can confidently approve after considering risk, underwriting, compliance, and long-term business viability.

How does trusted onboarding help reduce merchant onboarding risk?

Trusted onboarding brings together verification, risk scoring, merchant underwriting, customer due diligence, and approval workflows into a single process. This helps providers make more informed decisions and maintain consistent onboarding standards across the business.

Why does merchant onboarding become more difficult as providers grow?

As providers expand into new markets, products, and partner channels, they must manage different regulations, risk profiles, and onboarding requirements. Trusted onboarding provides a consistent framework for evaluating merchants while maintaining visibility, governance, and control at scale.

What capabilities support trusted merchant onboarding?

The most effective onboarding platforms combine KYB onboarding, KYC, AML screening, merchant underwriting, risk scoring, automated risk assessment, intelligent workflows, ongoing due diligence (OCDD), and centralized risk management into a single onboarding process. These capabilities help providers build a complete merchant risk profile, reduce merchant onboarding risk, and make more consistent onboarding decisions.