.png)

Merchant acquisition in payments is increasingly shaped by partner channels, not direct sales alone. Payment providers are using ISOs, software platforms, resellers, referral partners, and industry specialists to reach markets that would be difficult, slow, or expensive to access directly. This is partner-led merchant acquisition in practice: growth through trusted third-party relationships that already sit closer to the merchant.

The driver is trust. In many merchant relationships, confidence is built closest to the customer. A specialist partner may already understand the merchant’s sector, region, operating model, and day-to-day pressures. That relevance creates confidence faster than a generic sales process can.

But partner-led growth in payments only becomes a competitive advantage when local trust is backed by central governance. As providers scale through partners, they need consistent onboarding, KYB, KYC, AML, underwriting, approvals, and risk controls across every channel.

The strongest providers are not choosing between growth and control. They are building the infrastructure to scale partner-led merchant acquisition while maintaining visibility, consistency, and confidence in every onboarding decision.

Key Takeaways

- Partner channels create competitive advantage because they bring trust closer to the merchant through local relationships, sector expertise, and established customer networks.

- Direct sales is important, but it cannot credibly reach every niche, region, or embedded buying journey.

- As partner networks scale, payment providers need centralized governance across KYB, KYC, AML, underwriting, approvals, reporting, and OCDD.

- Governed onboarding infrastructure allows partners to preserve their market relevance while the provider keeps control of risk and compliance.

- White label merchant onboarding is not just branding. It is a way to turn local partner trust into a scalable, governed acquisition model.

Why direct sales alone cannot reach every merchant market

Most payment providers need direct sales. Internal teams understand the product, the value proposition, and the commercial model. But direct sales has a natural limit: it works best when the merchant already knows what they need and is actively looking for a solution.

A large share of the market is influenced long before a payment provider enters the conversation. Merchants may already trust a software provider, an ISO, a regional advisor, an equipment supplier, or a specialist operating in their sector. Those partners bring market context and relationship credibility that cannot be manufactured centrally.

The economics reinforce the point. Building direct sales coverage across every region and vertical requires salaries, commissions, SDR support, marketing, travel, enablement, and management overhead. Partner channels can share that acquisition burden while opening routes into markets a central sales team may struggle to reach alone.

The broader market data supports this shift. Crossbeam’s partner ecosystem research reports that deals are 53% more likely to close and close 46% faster when a partner is involved. Some partner-marketing benchmarks also report that 72% of companies see lower customer acquisition costs from partners compared with direct acquisition. At a macro level, Forrester, citing WTO, notes that 75% of world trade flows indirectly.

Indirect channels are no longer a secondary route to market. They are a major part of how buyers discover, evaluate, and choose providers.

Why partner channels win: trust is local, specific, and embedded in the buying journey

Embedded payments show why partner channels work. A childcare operator is not usually shopping for payments first. They are looking for software that helps them run their center. A gym owner may start with membership management. A vending operator may start with equipment. In each case, payments are part of the broader business need, and the most trusted route to that merchant is often the provider already solving the primary problem.

That is where partner channels create an advantage. The trusted partner already understands the merchant’s operating reality, commercial pressures, and buying context. They are not entering as a standalone vendor. They are expanding an existing relationship. Before a merchant evaluates a payment solution on features, they are already assessing whether they trust the person introducing it. Forrester research reinforces the same point: more than 90% of respondents said buyers trust peers in their industry, while vendor salespeople were the least trusted source tracked at 29%. That gap is structural, not situational.

Buyers naturally place more confidence in people who understand their world than someone they see as simply selling a product. In many markets, that understanding sits closer to the customer than it does to the provider.

Partners carry that trust into the sale. They understand the merchant's sector, operating constraints, and day-to-day realities. A partner serving gym operators knows what actually drives their decisions. A regional specialist understands local market conditions in a way a centralized sales team rarely can.

In some cases, trust extends beyond expertise into alignment. Partners often share geography, community ties, or even values with their customers, something a centralized sales function can't easily replicate or manufacture.

The scale implications are significant. McKinsey reports that vertical-specific software solutions captured more than 50% of US SME spending in 2023, showing how strongly merchant acquisition is moving toward embedded and vertical-specific buying journeys. Its more recent ISV research also shows that US payment-processing revenue through ISVs has grown 20% annually for the past five years, with the ISV channel growing three times as fast as traditional channels. Flagship Advisory Partners estimates that around 40% to 65% of newly signed US SMB merchants now source payment acceptance or acquiring through ISVs. Taken together, the data shows how strongly merchant acquisition is moving toward software platforms, specialist providers, and embedded buying journeys.

As Daniel Sheahan, CEO of MVSI, puts it: "The single biggest value of specialist partners is access to customers you can't reach directly." That access is not only about reach. It is about relevance. Whether the merchant sits in a niche industry, a regulated sector, a regional market, or a values-aligned community, specialist partners bring the local knowledge, industry credibility, social alignment, and trust that make merchants more willing to engage.

The result isn't just expanded reach; it's transferred credibility. Partners bring trust that providers often cannot establish directly, helping merchants feel more confident in the decision-making process.

We explore these challenges in more detail in our 20-minute webinar, How Payment Providers Scale Partner-Led Growth Without Losing Control, including why partner channels succeed, where visibility and control start to break down, and how payment providers can support partner growth without compromising governance.

Where partner-led growth creates risk

Distributed partner networks create reach, but they also create distance. The further the provider sits from the merchant relationship, the harder it becomes to maintain consistent visibility, data quality, risk assessment, and compliance control.

Every payment provider partner channel faces the same structural risk. But in payments, the consequence isn’t just brand inconsistency, it’s regulatory exposure. This principle is reflected in FATF’s third-party reliance framework: financial institutions may rely on third parties for certain customer due diligence measures, but accountability for those measures remains with the institution relying on the third party. In practice, this means responsibility remains with the payment provider, regardless of which partner originated or onboarded the merchant.

As partner ecosystems scale, the risk surface expands beyond AML and fraud. Providers also need to manage brand exposure, credit risk, scheme compliance, pricing integrity, product suitability, operational friction, and reputational impact. The underlying issue is consistent: greater distance between provider and merchant reduces execution consistency across every control layer.

The dominant failure mode is rarely intentional misconduct. More often, it is operational inconsistency across partner onboarding, compliance, and risk processes. Inconsistent reseller onboarding can mean different partners collecting different data, applying different standards, using different processes, and leaving compliance teams with a fragmented view across the portfolio. The channel might be scaling, but the governance isn’t following.

The solution isn’t to collapse back into direct control, which would reintroduce the cost and friction the model is designed to avoid. The challenge is more precise: how to maintain centralized governance while preserving partner-led execution?

Quiet control: how strong partner channels governed at scale

The strongest partner-led growth models do not scale by forcing every merchant interaction back through head office. They scale by embedding the right controls into the channel, so partners can move quickly while the provider maintains visibility, consistency, and governance. Strong partner channels do not bypass compliance. They build merchant trust through consistent, governed onboarding.

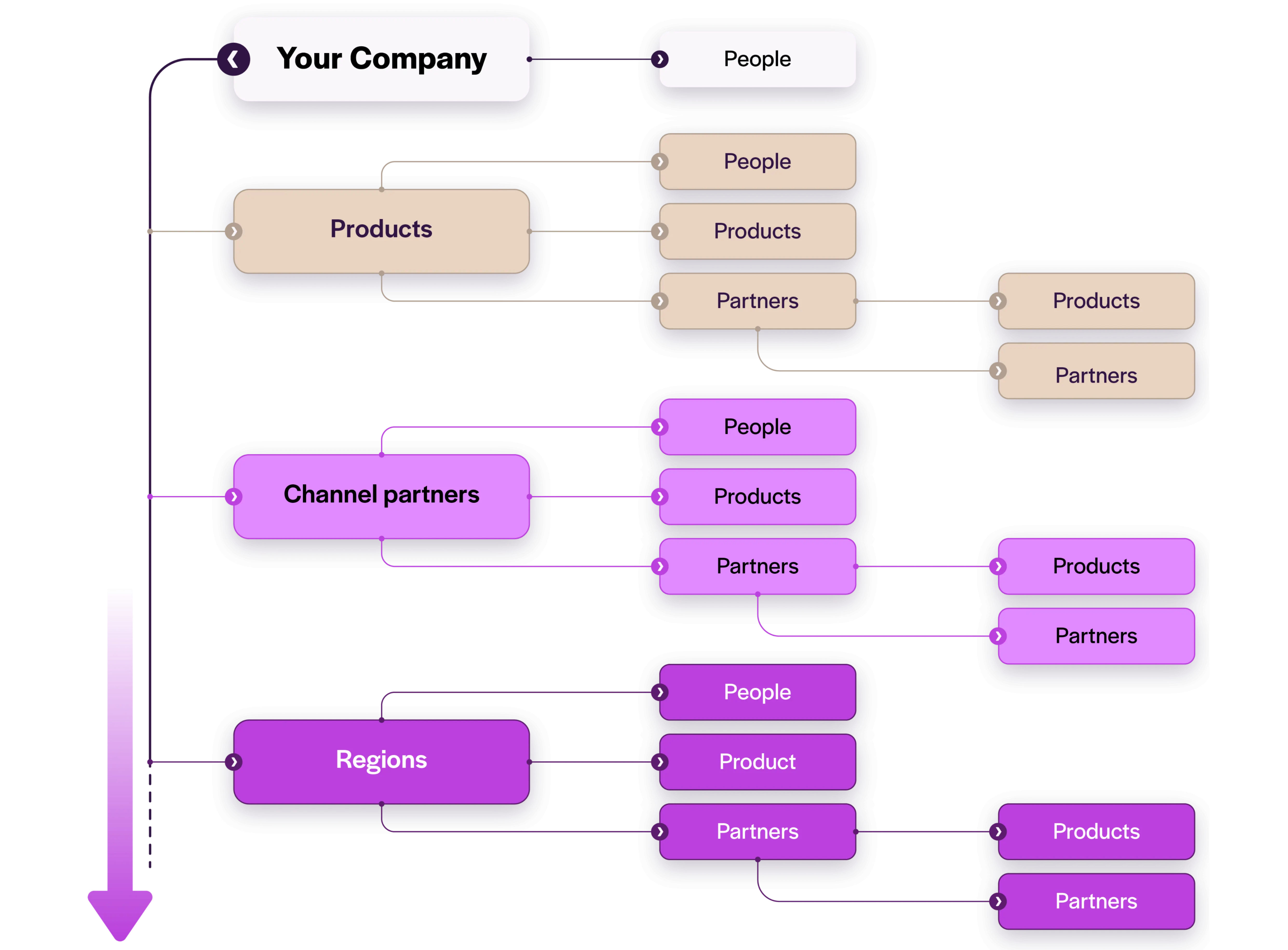

In partner channels merchant acquisition, governed onboarding infrastructure is what makes this balance possible. It doesn't replace the partner's relationship with the merchant. Instead, it allows partners to onboard merchants within a framework defined by the provider. Every onboarding journey should apply the right data requirements, document checks, risk criteria, underwriting rules, KYB, KYC, AML screening controls, approval workflows, and audit standards, regardless of which partner originates the application. Partners maintain ownership of the merchant relationship and onboarding experience, while providers retain oversight over how onboarding decisions are made. The goal is what might be called quiet control: governing consistently across every channel without introducing friction, cost, or delay.

centralized control across products, partners, and regions.

That is also what makes the shift from verified onboarding to trusted onboarding possible at scale. Verified onboarding confirms that individual checks have passed. But a merchant can pass individual checks and still create risk if the product, partner source, pricing, operating model, or broader compliance context does not make sense. Trusted onboarding brings those signals together so the provider can make a defensible decision, not just complete a checklist.

End-to-end white label merchant onboarding is the bridge between local partner trust and central provider control. The value is not simply branding. It is giving partners a merchant-facing journey that reflects their own market relevance, while the parent provider maintains the standards, controls, products, pricing, permissions, risk rules, and decisioning framework behind the scenes. The commercial value is not only that partners can sell under their own brand. It is that the provider can offer partners a trusted, branded route to market while keeping the controls that protect the business.

Putting a logo on a form is not white label onboarding. It is rebranding. A merchant receiving a generic application form with an unfamiliar brand isn't experiencing a localized journey, they're experiencing a corporate one with a different header. Genuine white label onboarding creates continuity between the partner relationship and the onboarding experience. The merchant remains within a familiar environment, while the provider maintains consistent governance behind the scenes.

Regardless of geography, language, or market context, every partner journey operates to the same standards. The partner brings the trusted relationship. The provider retains control of the risk decision.

This is the model OnBoard by MVSI was built to support. OnBoard is an end-to-end merchant onboarding and compliance platform that brings digital applications, offers, KYB, KYC, AML screening, underwriting, approvals, reporting, and ongoing due diligence into one governed workflow.

For partner-led growth, OnBoard gives providers a way to support white label merchant onboarding across partner networks while keeping compliance, risk, approvals, and visibility centrally controlled. In practice, one provider used OnBoard to build a reseller network of more than 100 partners, reduce onboarding time by 98%, and support more than 8,000 new merchant relationships, with compliance and risk governance maintained centrally throughout.

That is not growth despite governance. It is growth made possible by governance.

By standardizing onboarding and compliance requirements across every partner channel, providers can reduce operational risk, improve underwriting consistency, and maintain greater visibility into merchant onboarding activity across their ecosystem.

The future of partner-led growth is trusted onboarding at scale

Partner-led merchant acquisition succeeds because trust is built closest to the merchant. Specialist partners, software platforms, ISOs, resellers, and regional experts can create relevance and credibility that direct sales alone cannot replicate.

But in regulated payments, trust cannot stop at the relationship. The provider still needs consistent onboarding, compliance, underwriting, approvals, risk management, and ongoing oversight across every channel.

The most successful payment providers will be the ones that combine local partner trust with central governance. They will give partners the freedom to win merchants in their own markets, while keeping the controls needed to make trusted onboarding decisions at scale.

Ready to scale partner-led merchant acquisition without losing control?

Book a White Label Channel Growth Review now to explore where your channel model could increase merchant acquisition, improve visibility, and reduce compliance friction.

Disclaimer: This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or business advice. Regulatory obligations vary by jurisdiction, industry, and business model. Organizations should consult qualified legal, compliance, and risk professionals when designing or updating onboarding, KYB, KYC, AML, underwriting, and risk management processes.

Frequently Asked Questions

What is partner-led merchant acquisition?

Partner-led merchant acquisition is a growth model where payment providers acquire merchants through trusted third-party channels such as ISOs, software platforms, resellers, referral partners, and industry specialists. It helps providers reach markets, regions, and merchant communities that direct sales teams may struggle to access alone.

Why use partner channels for merchant acquisition?

Partner channels help payment providers reach merchants through existing relationships, local knowledge, sector expertise, and trusted routes to market. They can reduce acquisition burden and expand reach, especially in niche, regional, embedded, or specialist markets.

What makes a specialist or local partner more effective than direct sales in some markets?

Specialist partners often understand the merchant’s primary business need before payment enters the conversation. In embedded payments, unattended payments, vertical software, or regional markets, the merchant may already trust the partner providing the core solution. That makes the partner a more natural route into the relationship.

What compliance risks do partner channels create?

Partner channels can create compliance risk when onboarding data, KYB, KYC, AML checks, underwriting, approvals, or risk processes are applied inconsistently across partners. Even when a partner originates the merchant relationship, the provider still needs visibility and control over the onboarding decision.

What is white label merchant onboarding, and why does it matter?

White label merchant onboarding allows partners to present a branded merchant onboarding journey while the parent provider keeps control over products, pricing, permissions, KYB, KYC, AML, underwriting, approvals, reporting, and OCDD. It matters because it helps partners build merchant trust while the provider maintains governance.

How do payment providers maintain compliance control across a large partner network?

Payment providers can maintain control by using a governed onboarding platform that applies consistent rules, permissions, KYB, KYC, AML checks, risk scoring, approvals, reporting, and OCDD across partner-originated applications. The goal is to let partners move quickly while keeping risk and compliance decisions visible and defensible.

What is the difference between verified onboarding and trusted onboarding?

Verified onboarding confirms that individual checks have passed. Trusted onboarding looks at the full merchant context, including business profile, product fit, partner source, KYB, KYC, AML, underwriting, risk, approvals, and ongoing monitoring, to decide whether the merchant should move forward with confidence.