.png)

Business lending onboarding is where Australian lenders collect, verify, and assess the information needed to support funding decisions. When onboarding brings together business verification, customer due diligence, AML/CTF compliance, and risk assessment, it creates a stronger foundation for consistent, informed, and defensible lending decisions.

Lenders are under increasing pressure to approve applications faster while maintaining strong verification, compliance, and risk management controls. Balancing speed and control has become one of the biggest challenges in modern business lending.

As documentation requirements, due diligence obligations, and customer expectations continue to grow, onboarding has become a critical part of the lending process. The quality of onboarding can directly influence operational efficiency, risk management outcomes, and the customer experience.

This article explores how business verification, customer due diligence, and AML/CTF compliance shape lending decisions, the challenges traditional onboarding creates, and how Australian lenders can build more scalable onboarding processes.

Key Takeaways

- Business lending onboarding is more than document collection. It brings business verification, risk assessment, customer due diligence, and compliance controls into the lending decision process before funding is approved.

- Business verification, customer due diligence, and AML/CTF checks help lenders understand who they are lending to and make more informed decisions.

- Manual onboarding processes can create delays, increase workloads, and make it harder to maintain consistent compliance and risk controls.

- Bringing data collection, verification, compliance, and risk assessment together into one process can help improve efficiency and reduce operational friction.

- Lenders looking to scale need onboarding processes that support faster decisions without compromising compliance, risk management, or customer experience.

What is business lending onboarding?

Business lending onboarding is the process Australian lenders use to collect borrower information, verify businesses and owners, assess risk, complete customer due diligence, and prepare applications for lending decisions.

It sits between a business applying for finance and a lender deciding whether to approve funding. During onboarding, lenders may collect business details, ownership information, identity documentation, financial records, and risk indicators before progressing the application through internal review and approval workflows.

As business lending becomes more complex, business onboarding plays an increasingly important role in helping lenders maintain consistency, improve operational efficiency, and create a smoother experience for borrowers.

For many Australian lenders, onboarding is no longer just an administrative step. It has become the foundation for trusted lending decisions, helping lenders balance operational efficiency, regulatory compliance, and risk management from the very start of the customer relationship.

How business verification and AML/CTF compliance shape lending decisions

Australian lenders support a wide range of business finance products, each with its own onboarding, verification, and risk assessment requirements.

These may include:

- Business loans

- Lines of credit

- Business overdrafts

- Hire purchase agreements

- Invoice finance and invoice factoring

- Trade finance

Depending on the lending product, lenders may also review information relating to whether the loan is secured or unsecured, including any collateral or security provided, guarantor arrangements, and the purpose of the funding being sought.

Collecting this information is only the first step. Lenders must also:

- Validate that the information provided is accurate

- Confirm the identity of individuals associated with the application

- Understand who ultimately owns or controls the business

- Apply appropriate compliance and risk controls before funding can proceed

These requirements form the foundation of business lending onboarding and directly shape how lenders approach verification, due diligence, and compliance.

The following sections outline how business verification, customer due diligence, and AML/CTF compliance are applied in practice to support lending decisions.

Business verification as a lending control

Before lenders can assess risk, they first need confidence that the business is legitimate and that the information provided during onboarding is accurate.

Business verification helps lenders confirm that a business is legitimate, validate key information provided during onboarding, and build a clearer understanding of the organisation before progressing an application.

Depending on the product and borrower profile, lenders may also review business plans or other information that helps them assess:

- What the business does

- Who its customers are

- Its market position

- Growth opportunities

- Potential risks

To validate the information provided, lenders may also conduct:

- ABN verification

- ACN verification

- Director verification

- ASIC record checks

- Know Your Business (KYB) checks

Together, these checks help lenders verify key business information before progressing an application through the lending process.

Customer due diligence and beneficial ownership verification

Customer due diligence helps lenders identify the individuals behind a business and understand who ultimately owns or controls it.

Depending on the business structure, this may involve reviewing:

- Directors

- Shareholders

- Beneficial owners

- Ultimate Beneficial Owners (UBOs)

- Trustees and trust structures

For some lending products, lenders may also require information about an individual's financial position, including:

- Income tax returns

- ATO Notices of Assessment

- Assets and liabilities

- Existing loans and financial commitments

These checks help lenders better understand ownership structures, identify potential risks, and assess applications more effectively.

AML/CTF compliance requirements

Alongside business verification and customer due diligence, many Australian lenders need onboarding processes that support Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) compliance particularly where they provide regulated services, designated services, or operate within reporting entity obligations.

AML/CTF obligations can vary depending on the lender, product, customer type, and whether the lender provides a designated service or operates as a reporting entity. AML/CTF controls help lenders assess risk, apply appropriate due diligence measures, and maintain oversight throughout the customer relationship.

This may include:

- Customer risk assessments

- Risk-based due diligence

- Ongoing customer due diligence (OCDD)

- Record keeping

- Audit trails

Embedding these controls into the onboarding process helps lenders apply compliance requirements more consistently while supporting stronger risk management and operational efficiency.

Together, these controls help lenders make more informed lending decisions while supporting stronger risk management and compliance.

However, as application volumes increase, applying these controls consistently becomes more difficult. What works for a small lending operation often becomes harder to manage as documentation requirements, compliance obligations, and customer volumes grow.

Why traditional business lending onboarding creates operational and compliance challenges

Business lending onboarding requires lenders to collect and assess a wide range of information before funding can be approved.

The challenge is not simply collecting this information. It is ensuring that verification, due diligence, compliance, and risk assessment activities can be applied consistently without slowing lending operations down.

The pressure usually appears in four areas: documentation, team coordination, visibility, and scalability.

Growing documentation requirements

Business lending is often a document-intensive process. Information may need to be collected from multiple stakeholders and reviewed across different stages of the application.

This can create challenges when:

- Documents are submitted in different formats

- Information is incomplete or outdated

- Additional evidence is required during assessment

- Supporting records need to be manually reviewed

As document volumes increase, lenders can spend more time collecting and validating information than assessing applications.

Operational complexity across teams

Business lending onboarding often involves multiple teams, including operations, credit, risk, and compliance.

When onboarding activities are managed through emails, spreadsheets, and disconnected systems, it can become difficult to maintain a consistent process across every application.

This may result in:

- Duplicate reviews

- Manual handoffs between teams

- Delays in decision-making

- Inconsistent application handling

- Increased administrative effort

Over time, operational complexity can impact both efficiency and customer experience, making it more difficult for lenders to scale onboarding processes while maintaining consistency and compliance. The more stakeholders involved, the greater the need for structured onboarding workflows.

Reduced visibility and governance

Traditional lending onboarding processes can also make it harder to maintain oversight of applications as they move through the lending lifecycle.

Without a centralised view of onboarding activity, lenders may struggle to:

- Track application progress and ownership

- Monitor outstanding requirements

- Demonstrate how lending decisions were made

- Maintain complete audit records

As lending volumes grow, limited visibility can create governance challenges while making it harder to identify friction points, improve the borrower experience, and reduce application drop-off throughout the onboarding process.

Difficulties scaling onboarding operations

As lending operations grow, onboarding becomes more difficult to manage consistently. Different lending products often require different levels of verification, documentation, due diligence, and risk assessment.

Manual processes can make it harder to manage increasing application volumes efficiently. Onboarding teams may need to expand alongside growth, increasing staffing costs and operational overhead just to keep applications moving. Over time, this can create bottlenecks that slow decision-making, increase costs, and make growth more difficult to scale.

Rushing onboarding activities to keep pace with demand can also create risk. Incomplete reviews, inconsistent decisions, and gaps in risk assessment can make it harder to maintain consistent lending standards across a larger portfolio.

What works at lower volumes can quickly become difficult and expensive to maintain at scale. To support sustainable growth, lenders need onboarding processes that can handle increasing demand while maintaining consistent verification, risk, and compliance standards across every application.

How Australian lenders can strengthen business lending onboarding

The goal is not simply faster processing. Australian lenders need onboarding workflows that reduce operational friction while preserving confidence in the data, compliance controls, and lending decisions behind every application.

To improve efficiency without compromising compliance or risk management, lenders need onboarding processes that connect data collection, verification, due diligence, and decision-making into a single workflow.

For lenders operating in regulated financial services, platforms such as OnBoard by MVSI are designed to connect digital onboarding, KYB, AML/CTF screening, risk assessment, underwriting workflows, audit trails, and ongoing customer due diligence within a single operational framework.

Structured and dynamic data capture

The quality of an onboarding process is often determined by the quality of the information collected at the start.

Many onboarding delays can be traced back to incomplete, inconsistent, or inaccurate information captured at the start of the process. Capturing the right information upfront is one of the most effective ways to reduce rework, accelerate assessments, and improve the overall onboarding experience.

Rather than relying on static application forms, lenders can use dynamic onboarding form journeys that adapt in real time based on applicant responses.

Key capabilities include:

- Structured data capture that standardises information for assessment and decision-making

- Automated collection of information required across portfolios, products, or borrower types

- Real-time validation to identify missing or incorrect information before submission

- Personalised onboarding journeys that reduce unnecessary questions and application friction

Capturing complete and accurate information at the point of entry improves data quality, streamlines downstream processes, and creates a more personalised onboarding experience that can help reduce application abandonment.

for borrower information, verification, and onboarding.

Embedded compliance and risk-based due diligence

Verification alone is not enough. Lenders also need confidence that compliance, due diligence, risk rules, escalation pathways, and approval workflows are being applied consistently across every application.

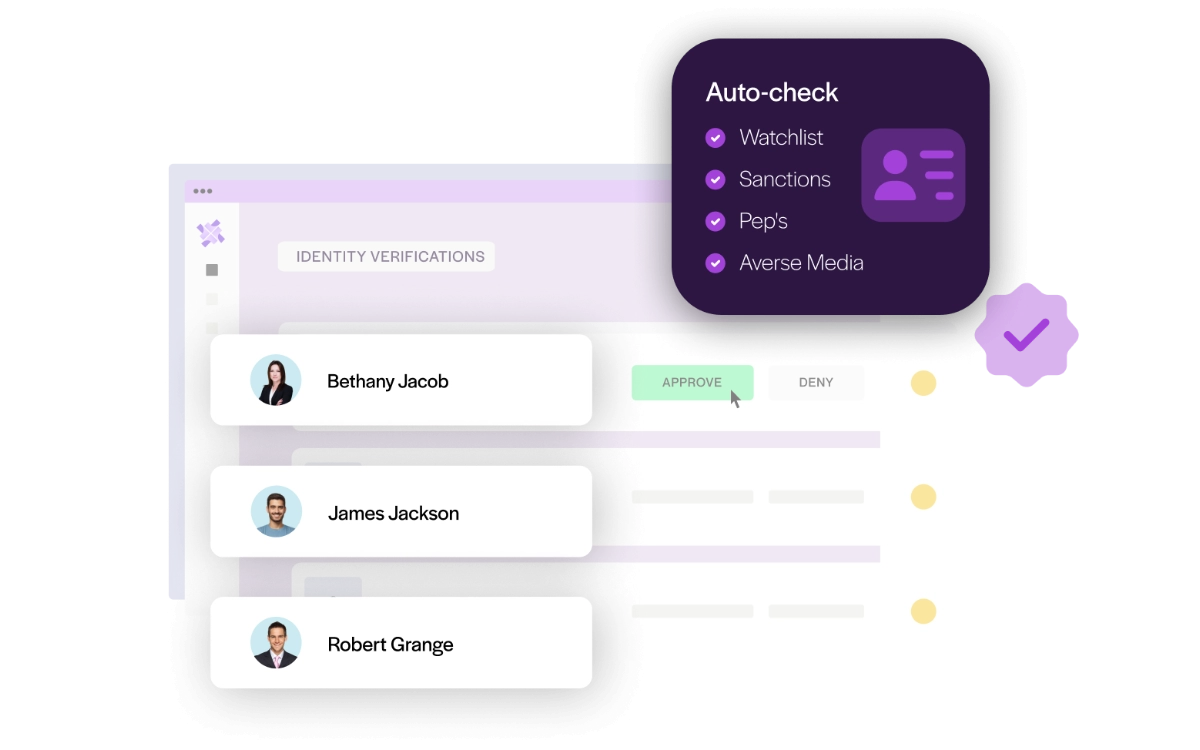

Know Your Business (KYB), Know Your Customer (KYC) and Anti-Money Laundering (AML) should be embedded into automated, risk-based workflows. This helps ensure that verification, screening, escalation, and review activities are applied consistently based on the applicant, lending product, and risk profile, rather than relying on manual processes.

Key capabilities include:

- Automated KYB and KYC workflows

- AML monitoring

- Automated PEPs and sanctions screening

- Customisable risk-based workflows by portfolio and product

- Ultimate beneficial ownership identification and verification

- Automated escalation pathways for higher-risk applications

Embedded compliance and due diligence workflows make it easier to apply controls consistently, reduce manual intervention, maintain oversight, and support more confident lending decisions.

Real-time document and data verification

Collecting onboarding documents is only the first step. Lenders also need to review information, extract key data, and determine what actions should happen next.

As document volumes increase, manual document reviews can slow applications down and create bottlenecks across lending operations. Real-time document intelligence helps streamline this process by reading and interpreting documents as they are submitted, extracting structured data, validating information, and triggering the next action automatically.

This reduces repetitive manual work, improves data quality, and gives teams greater confidence in the information being used to support lending decisions.

With verified data available earlier in the onboarding process, lenders can move applications forward faster and create a stronger foundation for risk assessment and underwriting.

Automated risk assessment and underwriting

Once onboarding data has been extracted, validated, and structured, it can be used to support risk assessment and underwriting decisions earlier in the lending process.

With complete and verified information available in real time, lenders can assess risk more consistently and apply underwriting criteria across different lending products, customer profiles, and risk levels.

Structured onboarding data supports automated risk scoring, policy checks, and application routing, helping ensure decisions are based on the same standards across every application.

This improves consistency, reduces turnaround times, and allows underwriting teams to focus on more complex or higher-risk applications.

Continuous monitoring and portfolio-level compliance

Risk management does not end once a loan has been approved.

Business circumstances, ownership structures, and risk profiles can change over time, making ongoing monitoring an important part of the lending lifecycle. By maintaining current customer information and continuously monitoring for changes, lenders can identify emerging risks earlier and respond more effectively when additional review is required.

Ongoing monitoring supports ongoing customer due diligence (OCDD), strengthens portfolio oversight, and keeps customer records accurate throughout the lending relationship.

Real-time reporting and full auditability

As lending operations grow, maintaining visibility across onboarding, compliance, and underwriting activities becomes increasingly important.

Real-time reporting and audit trails provide a clear record of how applications have been processed, what checks have been completed, and how lending decisions have been reached. This gives lenders a clearer view of how decisions were made and creates stronger support for governance, compliance, and internal oversight.

With access to accurate and up-to-date operational data, lenders can identify bottlenecks, monitor performance, and maintain stronger control across the lending lifecycle.

This centralised model can also support partner-led growth. For lenders that receive applications through brokers, referral partners, aggregators, or regional specialists, white label capabilities can help deliver a consistent branded borrower journey while keeping verification, AML/CTF controls, risk policies, approvals, workflows, and reporting centrally managed.

Building a scalable business lending onboarding framework

Business lending onboarding is no longer just about collecting documents and approving applications. Lenders are expected to verify businesses, understand ownership structures, assess risk, meet AML/CTF obligations, and maintain ongoing oversight throughout the customer lifecycle.

As lending volumes grow, maintaining consistency across verification, compliance, underwriting, and risk assessment becomes increasingly challenging. Processes that work at lower volumes can quickly become difficult to manage as application complexity, documentation requirements, and compliance obligations increase.

Creating a scalable onboarding framework requires lenders to bring verification, due diligence, underwriting, and ongoing monitoring into a connected process that supports both operational efficiency and stronger lending decisions.

OnBoard by MVSI is an end-to-end merchant onboarding and compliance platform for regulated payments, fintech, and financial services, combining digital onboarding, KYB, AML screening, underwriting, and ongoing due diligence (OCDD) in one system. By bringing business verification, customer due diligence, compliance screening, underwriting, and ongoing monitoring together, lenders can create a more consistent, scalable, and efficient approach to business lending onboarding.

Disclaimer: This article is provided for informational purposes only and does not constitute legal, financial, lending, compliance, or risk management advice. Business lending requirements, AML/CTF obligations, and verification processes may vary depending on the lender, product type, and regulatory requirements. Organisations should seek appropriate professional advice when designing or reviewing lending and compliance processes.

Frequently Asked Questions

What is business lending onboarding in Australia?

Business lending onboarding in Australia is the process lenders use to collect borrower information, verify businesses and owners, assess risk, complete customer due diligence, and prepare applications for lending decisions. It can include ABN verification, ACN verification, KYB checks, AML/CTF screening, risk assessment, underwriting workflows, and ongoing customer due diligence.

Why is business verification important in business lending?

Business verification helps lenders confirm that a business is legitimate and that the information provided during onboarding is accurate. This may include ABN verification, ACN verification, director verification, ASIC record checks, and Know Your Business (KYB) checks. These checks help lenders assess risk, support compliance requirements, and make more informed lending decisions.

How do AML/CTF obligations apply to business lending in Australia?

Many Australian lenders need onboarding processes that support anti-money laundering and counter-terrorism financing (AML/CTF) obligations, particularly where they provide regulated services, designated services, or operate as reporting entities. This may include customer risk assessments, risk-based due diligence, ongoing customer due diligence (OCDD), record keeping, and audit trails. Embedding these controls into onboarding workflows helps lenders maintain compliance while strengthening risk management and oversight.

Why do traditional business lending onboarding processes create operational challenges?

Traditional onboarding processes often rely on manual document collection, emails, spreadsheets, and disconnected systems. As application volumes increase, these processes can create delays, increase operational workloads, reduce visibility, and make it more difficult to apply verification, compliance, and risk controls consistently.

How does OnBoard by MVSI support business lending onboarding?

OnBoard by MVSI is an end-to-end merchant onboarding and compliance platform for regulated payments, fintech, and financial services, combining digital onboarding, KYB, AML screening, underwriting, and ongoing due diligence (OCDD) in one system. By bringing these activities together, lenders can create a more efficient, compliant, and scalable approach to business lending onboarding.

How can automated onboarding improve business lending operations?

Automated onboarding helps lenders reduce manual data entry, streamline verification and compliance checks, improve data quality, and accelerate application assessments. By connecting onboarding, verification, due diligence, and underwriting workflows, lenders can improve efficiency while maintaining consistent compliance and risk controls.

What is ABN verification in business lending?

ABN verification is the process of validating an Australian Business Number (ABN) to confirm that a business is registered and that the information provided during onboarding is accurate. Lenders often use ABN verification alongside other business verification and due diligence checks when assessing lending applications.