.png)

_%20What%20They%20Are.webp)

As financial crime grows more sophisticated, regulators are demanding greater clarity over who really owns, controls, and benefits from companies. For risk and compliance leaders, knowing exactly who owns or controls the entities they do business with is no longer optional. It’s a core part of Anti-Money Laundering (AML), Know Your Customer (KYC), and Customer Due Diligence (CDD) obligations.

At the centre of these efforts are Ultimate Beneficial Owners (UBOs) — the real people behind companies, trusts, and partnerships. Understanding and verifying them protects organizations from fraud, fines, and reputational harm.

Key Takeaways

- UBO identification is now a core compliance requirement under AML, KYC, and CDD frameworks worldwide.

- Knowing who truly owns or controls a business helps prevent money laundering, fraud, and tax evasion.

- A Beneficial Owner (BO) benefits financially from a company’s success, while an Ultimate Beneficial Owner (UBO) holds the highest level of control or influence.

- Global regulations are tightening, with new transparency laws like the EU’s AMLD5 and the U.S. Corporate Transparency Act (CTA).

- Automating UBO verification through platforms like OnBoard by MVSI improves accuracy, speeds onboarding, and reduces compliance risk.

What Is an Ultimate Beneficial Owner (UBO)?

A UBO is the natural person who ultimately owns or controls a company, even if their names do not appear in official or public records. UBOs are the real people who benefit from the company’s profits or hold the authority to make key decisions. They are the true beneficiaries behind corporate structures and identifying them is central to maintaining beneficial ownership transparency.

Finding a UBO often requires tracing through multiple layers of companies or entities to uncover who truly controls the business. In some cases, indirect or combined ownership across several entities may reveal an individual as the ultimate owner. Because corporate structures can be complex, identifying the UBO is not always straightforward, but it remains a legal requirement under KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations to ensure compliance and transparency.

Ownership thresholds vary by jurisdiction:

- In the European Union, the Fourth Anti-Money Laundering Directive (AMLD4) defines a UBO as someone with 25% or more ownership.

- Under SWIFT guidelines, thresholds can be as low as 10%, depending on risk profile and jurisdiction (SWIFT).

- The U.S. Corporate Transparency Act (CTA) defines a UBO as anyone with substantial control or 25% ownership (FinCEN CTA guidance, 2024).

Beneficial Owner vs. Ultimate Beneficial Owner

A Beneficial Owner (BO) is any person or entity that benefits financially from a company’s success. This may include receiving dividends, profits, or other financial returns. A BO holds ownership rights, typically through shareholding or equivalent means, but may not necessarily control how the company operates. Because shareholding can be divided among several people, a business can have multiple beneficial owners who each hold an economic interest.

An Ultimate Beneficial Owner (UBO), on the other hand, refers to the natural person or people who ultimately own a significant percentage of shareholding. Unlike a beneficial owner, a UBO may not directly hold shares but still exercises ultimate control through other means. Depending on how the organisation is structured, a company may have one or several UBOs who meet the relevant ownership or control thresholds.

When a company is represented by a trust, guardian, or another corporate entity, the UBO is the real person at the end of that chain — the individual on whose behalf the intermediary acts. This person may not appear in official filings but is the one who truly exercises influence over decisions and outcomes.

Although beneficial owners and ultimate beneficial owners serve different roles, both are critical to identify. Understanding who profits and who holds control provides a clearer picture of ownership structures and helps businesses meet beneficial ownership disclosure requirements. For AML purposes, most jurisdictions require identifying anyone with 25% or more ownership or control, though in higher-risk jurisdictions this threshold may be reduced to 10% or even 5%.

Recognizing both BOs and UBOs also supports stronger risk management. When you know who stands to gain and who controls decision-making, it becomes easier to detect conflicts of interest, prevent hidden ownership, and identify potentially suspicious financial activity.

Regular monitoring of both ownership types helps businesses stay alert to changes in structure. For example, a beneficial owner could acquire additional shares and become the UBO, shifting your exposure and compliance responsibilities.

If any beneficial owner appears on a Politically Exposed Persons (PEP) list, that individual may present corruption or bribery risks and should trigger enhanced due diligence procedures.

Why UBO Identification Matters for AML and Compliance

UBO verification is fundamental to preventing:

- Money laundering – Criminals often hide behind complex ownership chains.

- Terrorist financing – Anonymous entities make it easy to channel illicit funds.

- Tax evasion and corruption – Transparency ensures fair and legal financial conduct.

The Pandora Papers revealed how opaque shell companies concealed more than $11 trillion in offshore wealth worldwide, underscoring the scale of the issue.

Failure to perform due diligence can cost companies millions in fines — global regulators issued over $5 billion in AML-related penalties in 2023 alone.

The Global Regulatory Landscape

Different jurisdictions define and enforce UBO rules differently:

European Union:

AMLD4 and AMLD5 require companies to maintain Beneficial Ownership Registers, accessible to regulators and sometimes the public.

United States:

The Corporate Transparency Act (CTA) mandates that companies disclose beneficial ownership information to FinCEN beginning January 2024.

United Kingdom:

Companies must list individuals with more than 25% ownership or voting rights in the Persons with Significant Control (PSC) Register, along with the level of their shares and voting rights.

Australia:

AUSTRAC guidance defines a beneficial owner as any individual who directly or indirectly owns 25% or more of an entity and requires businesses to take “reasonable measures” to verify identity.

Understanding these regional variations is essential for multinational compliance strategies.

How to Identify and Verify a UBO

UBO identification is a key part of every strong AML and CDD framework. The process typically includes:

- Gather ownership information: Collect entity details such as registration number, legal structure, and ownership documentation.

- Trace indirect ownership: Review layered or trust-based ownership arrangements to uncover real control.

- Verify identity: Use independent, reliable data sources (such as corporate registries or verification APIs).

- Conduct CDD and KYC checks: Confirm accuracy and completeness of ownership information.

- Monitor continuously: Review UBO information periodically and whenever ownership changes occur.

Modern digital onboarding and KYB tools, like those offered by OnBoard by MVSI, can automate much of this process across jurisdictions, reducing manual effort and improving compliance accuracy.

Common Challenges in UBO Verification

- Complex ownership chains: Difficult to trace through multiple cross-border entities.

- Incomplete or outdated registries: Beneficial ownership data can be inaccurate or inaccessible.

- Manual verification inefficiency: Paper-based processes slow onboarding and increase risk of human error.

- Hidden ownership structures: Nominee shareholders and offshore trusts obscure control.

Identifying a UBO can take significant time when ownership spans multiple jurisdictions or corporate layers.

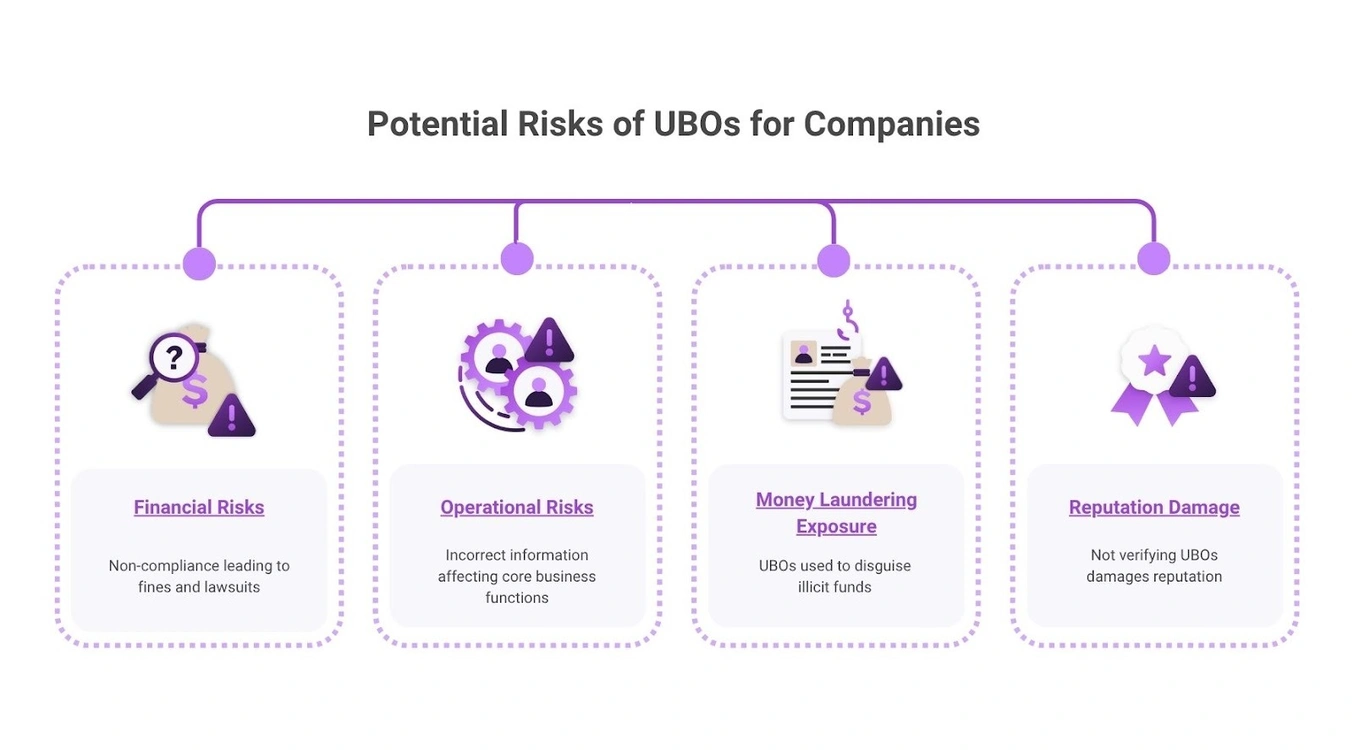

Failure to uncover the real owners behind a business doesn’t just delay compliance — it can expose organizations to serious risks.

These risks include regulatory fines, disrupted partnerships, and reputational damage if your organization unknowingly facilitates financial crime. In some cases, hidden UBOs have been linked to sanctions violations, bribery schemes, and money laundering investigations.

To reduce these risks, compliance teams are increasingly turning to automation and centralized data management. These tools consolidate ownership data from global registries, streamline verification, and deliver a single, reliable view of who truly owns or controls each entity.

The Role of KYC, CDD, and AML in UBO Compliance

Identifying the ultimate beneficial owner is not a standalone task, it plugs into a broader and continuous compliance framework that spans KYC, CDD and AML. Businesses that treat UBO checks as a one-off exercise may still leave gaps.

- KYC (Know Your Customer) verifies the identity of the entity or individual you are onboarding. It ensures you truly know who is on the other side of the relationship. This includes collecting verified identity documents and validating the individual’s legitimacy.

- CDD (Customer Due Diligence) moves beyond identity and assesses the underlying ownership structure and risk profile. It requires you to find out who profits from the business (beneficial owners) and who has ultimate control (UBO). Through CDD you ensure transparency over complex ownership chains, trust arrangements or nominee structures.

- AML (Anti-Money Laundering) is the ongoing monitoring and control mechanism. Once you have identified the BOs and the UBO, you must maintain vigilance: monitor for suspicious transactions, flag changes in ownership, re-verify when significant events occur, and report unusual activity.

Together these three elements form a continuous compliance cycle:

- Onboard with KYC → examine ownership with CDD → monitor activity via AML

- When ownership or control changes, revisit CDD, update your KYC records and ensure your AML monitoring reflects the new reality

- For example, when a beneficial owner buys more shares and becomes the UBO, the risk profile changes and your compliance treatment must adjust accordingly

Putting UBO identification at the heart of this cycle protects your organization from regulatory enforcement, financial loss and reputational hit. When you know both the people who benefit financially and the person who holds the ultimate control, you’re in a strong position to act if red flags arise.

Global Trends and What’s Next

Global regulators are expanding beneficial ownership transparency. Recent developments include:

- EU’s upcoming Anti-Money Laundering Authority (AMLA), centralizing AML supervision.

- The U.S. FinCEN Beneficial Ownership Information (BOI) database launching in 2024.

- The FATF’s continued push for cross-border data sharing and beneficial ownership transparency (FATF 2023 guidance).

Future-ready organizations are investing in automated verification tools that consolidate KYC, KYB, and UBO checks within unified platforms.

How OnBoard by MVSI Simplifies UBO Compliance

MVSI helps global organizations identify and verify Ultimate Beneficial Owners with confidence. Our platform brings AML, KYC, and KYB workflows together, ensuring accuracy, transparency, and compliance across 180+ jurisdictions.

See how MVSI helps reduce risk and accelerate compliance. Book a demo.

Frequently Asked Questions

What does UBO stand for?

UBO stands for Ultimate Beneficial Owner, the person who ultimately owns or controls a company or legal entity.

What is the UBO ownership threshold?

Typically between 5% and 25%, depending on jurisdiction (AUSTRAC, AMLD4).

Who enforces UBO compliance?

Depending on the country, enforcement is handled by agencies like FinCEN (U.S.), AUSTRAC (Australia), and the Financial Intelligence Units in the EU and UK.

Can a company have more than one UBO?

Yes. A company may have multiple UBOs if several individuals meet the ownership or control criteria.

How often should UBO information be updated?

Best practice is to review and update UBO information at least annually, or whenever ownership changes occur. (FATF guidance, 2023).