.png)

.webp)

KYC requirements in Australia help businesses comply with AML/CTF obligations through customer identity verification, due diligence, transaction monitoring, and technology-driven onboarding and compliance processes.

Know Your Customer (KYC) is not just a box-ticking exercise in Australia’s financial sector. It is the frontline defence against money laundering, fraud, and even terrorism financing. For many businesses, however, meeting these requirements can feel like a constant balancing act: juggling documentation, keeping pace with evolving regulations, and balancing customer experience with thorough checks.

The payoff is significant. When implemented well, KYC does more than protect against risks. It builds trust, improves efficiency, and creates a stronger foundation for growth. By embracing smarter processes and technology, compliance teams can spend less time on repetitive admin and more time on meaningful oversight, while leadership gains confidence that the business is both protected and scalable.

Key Takeaways

- KYC requirements in Australia help protect the financial system by preventing fraud, money laundering, and terrorism financing.

- Australia’s AML/CTF Act and AUSTRAC establish the regulatory framework for customer identity verification, transaction monitoring, and suspicious activity reporting.

- Businesses must apply strong customer due diligence, ongoing monitoring, and record-keeping practices to maintain compliance with evolving regulations.

- Technologies such as AI and automation can improve KYC efficiency, reduce operational workload, and strengthen compliance processes.

- Compliance officers play a critical role in overseeing KYC obligations and ensuring ongoing regulatory adherence.

What is KYC, and Why is it Important?

KYC requirements in Australia refer to the process businesses use to verify the identities of their clients. This is essential for preventing the facilitation of criminal activity, such as money laundering, fraud, and terrorism financing. KYC not only protects the financial system but also provides businesses with a foundation of trust that strengthens customer relationships and reduces long-term risk.

The key objectives of KYC are multi-faceted:

- Preventing Fraud: By verifying identities, businesses can confirm they are dealing with legitimate clients, protecting both their own interests and those of their customers.

- Ensuring Compliance: Financial institutions must adhere to stringent regulations aimed at preventing illegal activity. KYC supports compliance with both local and international AML and CFT obligations.

- Mitigating Financial Crime Risks: Early identification of high-risk customers helps businesses avoid exposure to criminal activity while protecting financial stability and reputation.

- Supporting Law Enforcement: KYC requirements in Australia provide important information that assists authorities in identifying and investigating financial crime.

While KYC is mandatory for regulated industries such as banks, fintech, and insurance, it also applies to sectors like real estate, legal services, and gambling. These industries are often involved in large transactions or complex structures, which can obscure illicit fund movements. Even businesses that are not legally required to implement KYC may choose to do so, as a proactive measure to reduce risks and protect their reputation.

In short, KYC is more than just a regulatory requirement; it's a vital practice for maintaining a transparent, secure, and trustworthy financial system.

Australia’s AML/KYC Regulatory Framework

Australia has put in place a solid framework for KYC compliance to reduce risks like money laundering, terrorist financing, and other financial crimes. At the heart of this is the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act), which requires thorough identity verification, transaction monitoring, and suspicious activity reporting to AUSTRAC.

At the same time, the Privacy Act 1988 ensures businesses handle customer data responsibly, keeping personal and financial details safe throughout the KYC process. This law outlines how data should be collected, stored, and used, ensuring businesses meet both KYC and privacy requirements. Together, these laws create a balanced approach, tackling financial crime while protecting privacy.

Additional regulations, like the Corporations Act 2001, which covers business entity identification, and AUSTRAC’s guidance notes, which provide clarity on how these laws should be applied, complement the AML/CTF Act. This comprehensive regulatory framework ensures businesses can meet KYC requirements while staying in line with broader legal and privacy standards.

Who Regulates AML/KYC Compliance?

In Australia, compliance with AML/KYC regulations is overseen by three key regulatory bodies: AUSTRAC, ASIC, and APRA.

- AUSTRAC (Australian Transaction Reports and Analysis Centre) is the main authority responsible for enforcing the AML/CTF Act. It monitors financial transactions, ensures businesses follow KYC procedures, and imposes penalties for non-compliance. AUSTRAC plays a crucial role in detecting and preventing financial crimes such as money laundering and terrorism financing.

- ASIC (Australian Securities and Investments Commission) focuses on corporate governance, financial services, and consumer protection. While its main focus is broader corporate conduct, it also works on KYC compliance, especially for businesses in financial services.

- APRA (Australian Prudential Regulation Authority) ensures the stability of the financial system and the health of financial institutions. Though it concentrates on the financial soundness of these institutions, its role overlaps with KYC requirements, particularly regarding institutional integrity.

Together, they monitor financial systems, enforce obligations, and align practices with international standards.

Key Components of KYC Compliance

To ensure effective KYC compliance, businesses must integrate several crucial components. These elements help in verifying customer identities, assessing associated risks, and maintaining ongoing vigilance to prevent financial crimes such as money laundering and terrorist financing.

Customer Identification Program (CIP)

The Customer Identification Program requires businesses to collect and verify personal details, such as name, date of birth, and address, using independent and reliable sources. This reduces fraud risk and builds confidence during onboarding.

Customer Due Diligence (CDD) & Risk Assessment

After confirming a customer's identity, businesses need to perform Customer Due Diligence (CDD) to assess the risks each customer may present. Not every client carries the same level of risk, and applying the same checks to everyone wastes resources. A risk-based approach ensures compliance teams focus effort where it truly matters. Customers are placed into different risk categories, and due diligence actions are adapted accordingly:

- Standard Due Diligence (SDD): Applied to lower-risk customers using routine verification and monitoring processes.

- Enhanced Customer Due Diligence (EDD): Applied to higher-risk customers, such as Politically Exposed Persons (PEPs) or customers from high-risk jurisdictions, requiring additional scrutiny and verification.

- Ongoing Customer Due Diligence (OCDD): Continuous monitoring of customer activity and transactions to identify suspicious behaviour or changing risk profiles.

By categorising customers based on their risk levels and applying the right due diligence measures, including enhanced customer due diligence for higher-risk customers, businesses can effectively mitigate potential risks while meeting regulatory requirements. Ongoing monitoring remains critical to spotting any irregularities that could point to fraudulent activities, keeping businesses proactive in protecting a secure financial environment.

For many teams, these checks are resource-intensive. Automating parts of the CDD process can help reduce manual workload, improve accuracy, and support more efficient ongoing monitoring.

The KYC Process in Australia

The KYC process in Australia is designed to protect businesses and the financial system by verifying both individual and corporate customers. It includes four key steps:

1. Identity Verification Requirements

To meet Australian regulations, businesses must verify their customers' identities using reliable, independent sources. This typically involves government-issued ID documents like passports, driver’s licences, and utility bills to confirm an address.

These documents must be checked for authenticity, with businesses required to have solid verification procedures in place to avoid fraud. Some businesses also use biometric tools, like facial recognition or liveness detection, to add an extra layer of security.

2. Know Your Business (KYB) Requirements

While KYC focuses on verifying individual customers, it is often used in conjunction with Know Your Business (KYB), this process involves verifying key details about the company, such as its name, address, and registration information.

Importantly, businesses must identify the Ultimate Beneficial Owner (UBO)—the person or group who ultimately controls or profits from the company. This helps uncover any risks tied to opaque ownership structures that could be used for activities like money laundering.

3. Record-Keeping Obligations

Businesses in Australia are required to maintain thorough records of the KYC process, keeping all customer identification details and transaction histories for at least seven years.

These records are vital for ongoing compliance and provide an audit trail in case of investigations or regulatory scrutiny. The long retention period highlights the importance of solid data management to reduce regulatory risk.

4. Suspicious Activity & Transaction Reporting

A key part of KYC requirements in Australia is reporting any suspicious transactions. Financial institutions must notify AUSTRAC of any unusual activities. Transactions related to terrorism financing must be reported within 24 hours, while other suspicious activities need to be reported within three business days.

Timely and accurate reporting is essential for preventing criminal activity and ensuring businesses don’t unintentionally support money laundering or terrorism financing.

This thorough KYC process is an essential part of Australia’s regulatory system, helping businesses stay compliant while contributing to global efforts to combat financial crime.

In practice, these KYC and compliance processes are increasingly managed within an end-to-end merchant onboarding platforms, where identity verification, KYB, transaction monitoring, and ongoing due diligence are handled as part of a unified workflow rather than separate systems.

Compliance Best Practices for Australian Businesses

Achieving and maintaining KYC compliance requires a strategic approach, balancing legal requirements with operational efficiency. Australian businesses can streamline their processes by following best practices designed to reduce risk while meeting regulatory standards. Here’s a breakdown of the key steps to ensure strong KYC compliance:

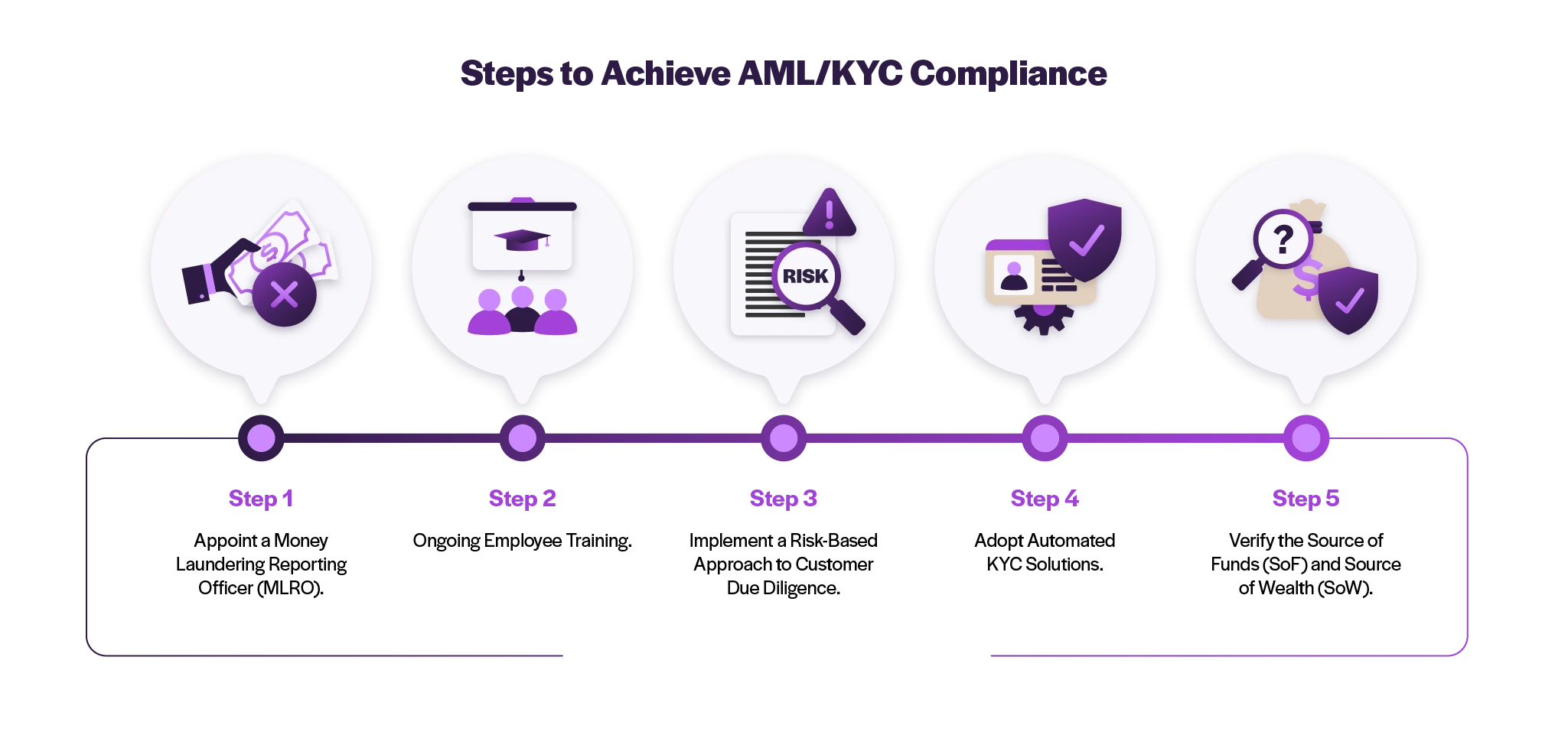

Steps to Achieve AML/KYC Compliance

1. Appoint a Money Laundering Reporting Officer (MLRO): The MLRO plays a key role in overseeing AML and KYC procedures. This person ensures compliance is maintained, flags suspicious activities in real time, and integrates any regulatory changes into business practices.

2. Ongoing Employee Training: Employees must be equipped to understand KYC regulations and their role in compliance. Regular training ensures staff can identify red flags, report suspicious activities, and stay informed about any changes to legal requirements.

3. Implement a Risk-Based Approach to Customer Due Diligence: Tailoring the due diligence process—including enhanced customer due diligence for higher-risk individuals and entities—to the risk level of each customer is essential. While low-risk customers might need basic verification, higher-risk customers (e.g., Politically Exposed Persons) require more thorough checks. This approach allows businesses to allocate resources effectively while staying compliant.

4. Adopt Automated KYC Solutions: Automation is critical to improving both efficiency and accuracy. Automated systems reduce the risk of human error, speed up customer verifications, and ensure compliance with the latest regulatory changes. AI-driven solutions can also help spot suspicious activities more effectively than manual checks.

5. Verify the Source of Funds (SoF) and Source of Wealth (SoW): For high-risk customers or cross-border transactions, confirming the SoF and SoW is vital. This ensures businesses can verify the legitimacy of customer transactions and avoid facilitating illicit activities.

Challenges in KYC Compliance

While current practices offer a solid compliance foundation, businesses still face several ongoing hurdles:

- Complex Ownership Structures: Verifying the true owners of intricate corporate entities, particularly shell companies, remains a significant challenge. To conduct thorough due diligence, businesses must fully understand the ownership structure, often requiring cross-referencing multiple sources of information.

- Managing High-Risk Customers: High-risk customers, such as PEPs or those from risk-prone regions, require enhanced due diligence and continuous monitoring. This can be resource-intensive, demanding constant attention to manage these relationships effectively.

- Adapting to Evolving Regulations: The regulatory environment for AML/KYC compliance is in a constant state of flux. Keeping up with changes in laws, AUSTRAC guidance, and international regulations is an ongoing challenge that requires businesses to remain flexible and proactive.

- Data Security and Privacy Concerns: Ensuring the secure storage of customer data in line with the Privacy Act is essential. This includes protecting personal and financial information, implementing robust security measures, and staying up to date with best practices in data storage and encryption.

By following these best practices, Australian businesses can not only meet their legal obligations but also foster a proactive, risk-aware culture that strengthens long-term compliance.

Penalties for Non-Compliance

Non-compliance with KYC regulations in Australia comes with heavy penalties for both individuals and businesses. Individuals who breach these regulations can face fines up to A$6.26 million and, in extreme cases, life imprisonment. For businesses, fines can reach as high as A$31.3 million, depending on the severity and scale of the violation.

These penalties highlight the seriousness of non-compliance, with high-profile cases serving as stark reminders of the risks companies face. For example, major financial institutions and fintech firms have been penalised for failing to adequately monitor transactions or properly verify customer identities. Beyond financial penalties, non-compliance can cause lasting reputational damage, undermining customer trust and potentially driving away business.

The stringent penalties and enforcement measures demonstrate Australia’s strong stance on tackling financial crime, ensuring that businesses and individuals alike recognise the importance of meeting KYC obligations.

Conclusion

KYC compliance is more than a regulatory burden. It is a safeguard for your business, your customers, and Australia’s financial system. Whether managing customer verification directly, overseeing compliance operations, or driving business growth, strong KYC practices deliver measurable operational and regulatory benefits.

By adopting a risk-based approach and leveraging modern merchant onboarding platforms with AI-driven verification, businesses not only stay aligned with the AML/CTF Act but also unlock real efficiency.

Note: This content is provided for general informational purposes only and does not constitute legal or regulatory advice. AML/KYC obligations may vary depending on industry, business model, and jurisdictional requirements.

Frequently Asked Questions

What is Customer Due Diligence (CDD) in KYC?

Customer Due Diligence (CDD) is the process of assessing customer risk by verifying identities, reviewing customer information, and monitoring transactions to identify potential money laundering or fraud risks. Higher-risk customers may require Enhanced Due Diligence (EDD) measures.

Is KYC required in Australia?

Yes, KYC is required in Australia under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act). Businesses in regulated sectors must verify customer identities, monitor transactions, and report suspicious activity to AUSTRAC to comply with AML and KYC obligations.

When was KYC introduced in Australia?

KYC requirements were formally established in Australia through the AML/CTF Act 2006, which introduced customer identity verification, transaction monitoring, and suspicious activity reporting obligations aligned with international AML standards.