.png)

KYB compliance helps financial institutions verify business legitimacy, identify Ultimate Beneficial Owners (UBOs), reduce financial crime risk, and support regulatory compliance. As fraud tactics become more sophisticated and onboarding expectations continue to rise, effective KYB programs combine verification, monitoring, and due diligence to strengthen trust and protect financial services operations.

For compliance and risk teams, the pressure is growing: merchants and corporate clients expect fast onboarding, regulators demand transparency, and fraudsters are using ever more sophisticated tactics. KYB has become essential not just for meeting rules, but for protecting operations and maintaining customer trust.

Key Takeaways

- KYB compliance for lenders helps financial institutions verify business identities, ownership structures, and Ultimate Beneficial Owners (UBOs) to reduce fraud, financial crime, and onboarding risk.

- Global and regional regulations, including FATF, FinCEN, and the EU’s AML directives, make strict due diligence mandatory to avoid penalties and reputational risks.

- Automation, AI, and real-time data access help streamline KYB processes, improve accuracy, and support scalable digital onboarding across financial services.

- Effective KYB programs combine verification, risk assessment, and ongoing due diligence to strengthen compliance and protect against evolving fraud threats.

What is KYB Compliance, and Why is it Important?

As fraud and financial crime become increasingly sophisticated, robust KYB processes are more important than ever.

According to a study by Juniper Research, online payment fraud is expected to exceed $362 billion globally between 2023 and 2028, with business impersonation scams playing a significant role. In 2023 alone, the US Federal Trade Commission reported over 330,000 instances of business impersonation scams, highlighting the urgent need for robust KYB measures. Every new business onboarded carries potential risks, from fraudulent shell companies to complex ownership structures designed to hide illicit activity.

Definition of KYB Compliance

KYB compliance is a due diligence process that involves verifying the identity, ownership structure, and legitimacy of business entities. It includes identifying Ultimate Beneficial Owners (UBOs), assessing the economic profile of the business, and ensuring compliance with Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) regulations. KYB is not just a regulatory requirement but a proactive measure to protect financial institutions from being exploited by fraudulent entities. For merchant onboarding, this ensures that only legitimate businesses gain access to financial services and payment infrastructure.

Why It’s Essential for Financial Services

KYB plays a critical role in:

- Preventing fraud – Fraudsters set up shell companies or impersonate legitimate businesses to access financial services. KYB processes, such as verifying business addresses and ownership structures, help flag suspicious entities before they cause harm. Verifying business addresses, licenses, and ownership structures helps compliance teams detect and block suspicious entities before they are onboarded.

- Reducing money laundering risks – Businesses can be used as fronts for illicit financial flows. Identifying and verifying UBOs ensures financial institutions aren’t unknowingly facilitating money laundering or terrorist financing.

- Maintaining compliance – Financial institutions are legally required to verify business customers and report suspicious activity. Non-compliance can lead to hefty fines, reputational damage, and loss of operating licenses.

How Does KYB Differ from KYC?

When onboarding clients, financial institutions follow different verification processes for individuals and businesses. KYC focuses on individuals, verifying basic identity details, while KYB investigates business structures and ownership. Understanding these distinctions helps manage risk, ensure compliance, and streamline onboarding:

KYB vs. KYC: Key Differences

- KYB (Know Your Business): Verifies businesses, including ownership structures, ultimate beneficial owners (UBOs), and legal status. This process is more complex due to corporate hierarchies and cross-border regulations.

- KYC (Know Your Customer): Verifies individuals, checking identity, address, and financial history. KYC is generally simpler, involving documents like passports or utility bills.

Why the Distinction Matters

While KYC is essential for onboarding customers, KYB is critical when dealing with corporate clients. The complexity of business structures—especially in cross-border transactions—makes KYB a more detailed process. Identifying UBOs in multi-layered organizations requires advanced due diligence, something KYC doesn’t typically involve. KYB also requires verification of business licenses, tax IDs, and financial statements, adding another layer of complexity.

Industry-Specific KYB Compliance Considerations

KYB industries are those exposed to financial crime, fraud, and regulatory scrutiny. Each sector has unique onboarding challenges that compliance and risk teams must address:

Banking & Fintech

- Real-Time Monitoring – Banks and fintech firms must track transactions live to flag suspicious activity and prevent financial crime.

- Enhanced Due Diligence – High-risk customers require deeper scrutiny to meet AML (Anti-Money Laundering) standards.

Crypto & Payments

- Stricter UBO Verification – Given the anonymity of blockchain, platforms must dig deeper to verify ownership structures and prevent fraudulent merchants from exploiting their systems.

Insurance

- Fraud Prevention – Accurate risk profiling and underwriting depend on verifying business legitimacy, reducing exposure to fraudulent claims.

Industries with high fraud risks and regulatory oversight require robust KYB processes to verify ownership structures, assess financial activities, and monitor transactions. Without them, businesses risk non-compliance, financial loss, and reputational damage.

Regulatory Frameworks Governing KYB Compliance

Staying compliant with Know Your Business (KYB) regulations is essential for managing financial risk. Businesses need to verify corporate clients, identify Ultimate Beneficial Owners (UBOs), and conduct due diligence to prevent financial crime. But KYB compliance isn’t straightforward—requirements vary by jurisdiction, making it a challenge for companies operating across borders.

Keeping up with evolving regulations is key to avoiding penalties, mitigating risk, and maintaining trust in the financial system:

Global and Regional Regulations

- FATF (Financial Action Task Force): Sets global AML standards, including KYB requirements. FATF guidance highlights the need to identify and verify UBOs to combat money laundering and terrorist financing.

- AUSTRAC (Australia): Imposes strict KYB obligations on financial institutions, requiring them to verify corporate clients and report suspicious activity.

- FCA (UK): Mandates thorough verification of business entities and UBOs to prevent financial crime and ensure compliance with AML laws.

- FinCEN (US): Enforces KYB compliance under the Bank Secrecy Act, requiring financial institutions to implement strong KYB measures.

- MAS (Singapore): Implements strict AML and CFT regulations, obliging businesses to verify corporate clients and report suspicious transactions.

Jurisdictional Differences: KYB regulations aren’t uniform, which makes compliance across multiple regions complex. The EU’s 5th and 6th AML Directives prioritize UBO transparency, while the US PATRIOT Act focuses on broader AML measures. For multinational merchant onboarding, risk teams must adapt KYB processes to different jurisdictions while keeping efficiency intact.

Challenges in KYB for Financial Institutions

Implementing KYB effectively is anything but simple. Financial institutions must keep up with evolving regulations, navigate complex corporate structures, and streamline client onboarding—all while maintaining rigorous due diligence. The challenges are compounded by the global nature of business and growing expectations for seamless digital experiences. Below are some of the key obstacles financial institutions face in their KYB processes.

Key Challenges

- Verifying Complex Corporate Structures – Identifying ultimate beneficial owners (UBOs) in multi-layered organisations is a time-consuming task. Financial institutions must untangle intricate corporate hierarchies to ensure compliance. For merchant onboarding, risk teams often need to untangle opaque ownership webs to catch hidden risks.

- Cross-Border Compliance – Navigating regulatory differences across jurisdictions is a constant challenge. Institutions must adapt their KYB processes to meet the specific requirements of each region in which they operate.

- Balancing Speed and Compliance – Onboarding needs to be efficient, but cutting corners on due diligence isn’t an option. Digital onboarding for banking helps financial institutions accelerate KYB without compromising regulatory standards. End-to-end onboarding solutions helps strike this balance, enabling faster merchant approvals without weakening controls.

How Digital Onboarding Enhances Compliance

Businesses need to balance speed and security, but traditional KYB processes often fall short. Manual verification is slow, labor-intensive, and prone to errors—creating delays and compliance risks at a time when financial crime is becoming more sophisticated.

Digital onboarding for merchants and corporate clients solves this by combining automation, AI, and real-time data. It makes KYB faster, more secure, and scalable.

Benefits of Technology

- AI-Powered Risk Assessment – Detects fraud and assesses risk in real time. AI can process large volumes of data, spotting anomalies and flagging suspicious activity instantly.

- Automated Verification – Speeds up business verification and UBO identification. Automated systems quickly and accurately check business documents and ownership structures. Automated systems reduce workload for compliance teams and ensure accuracy in merchant onboarding.

- Real-Time Data Access – Provides instant checks against global business registries, ensuring compliance with up-to-date business and UBO information.

Best Practices for Seamless KYB Compliance

Staying on top of KYB compliance means taking a proactive approach that balances regulatory requirements with operational efficiency. With financial crime becoming more sophisticated and regulatory expectations tightening, businesses need to verify entities quickly and accurately.

Recommendations

- Automate Risk Scoring – AI-driven risk assessments provide continuous monitoring, helping to identify high-risk clients and flag potential issues early.

- Use API-Driven KYB Solutions – Integrating KYB processes into existing systems improves efficiency, reduces friction, and ensures scalability.

- Keep Audit-Ready Documentation – Maintaining up-to-date, accessible records makes it easier to demonstrate compliance and respond to audits when needed.

Embedding these practices ensures KYB supports both regulatory compliance and faster merchant onboarding.

Role of Technology in KYB for Financial Services

Financial institutions need to balance efficiency with compliance in an increasingly complex regulatory environment. KYB processes are critical for verifying corporate entities, identifying Ultimate Beneficial Owners (UBOs), and managing financial crime risks.

But traditional KYB methods—manual checks, paperwork, and scattered data sources—are slow, error-prone, and difficult to scale. As regulations evolve and transaction volumes grow, financial services firms are adopting technology-driven solutions to improve verification, accuracy, and risk management.

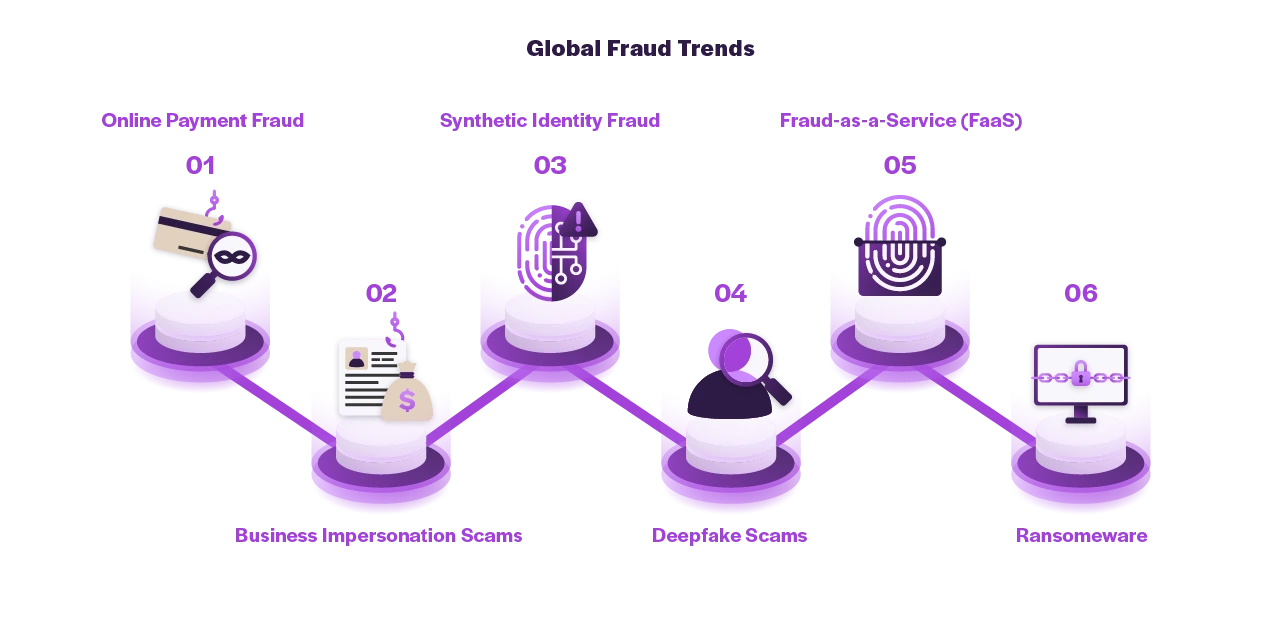

Global Fraud Trends & KYB’s Role in Prevention

Fraud is becoming more sophisticated, with businesses facing increasingly complex threats. Ongoing KYB monitoring and customer due diligence are critical for identifying emerging threats such as synthetic identities, deepfakes, and business impersonation scams.

Rising Fraud Trends

- Online Payment Fraud: Expected to exceed $362 billion globally (2023-2028). Fraudsters are increasingly targeting online payment systems.

- Business Impersonation Scams: Over 330,000 cases reported in the US in 2023. Fraudsters impersonate legitimate businesses to deceive victims.

- Synthetic Identity Fraud: A growing threat where criminals combine real and fake information to create fraudulent identities, often used to open bank accounts, apply for loans, or commit financial fraud.

- Deepfake Scams & AI-Powered Fraud: Fraudsters are using AI-generated deepfake videos, voice clones, and manipulated documents to bypass identity verification, making fraud detection more difficult.

- Fraud-as-a-Service (FaaS): Organized cybercriminal networks now offer fraud tools, stolen data, and automated attack services, making it easier to commit financial fraud at scale.

- Ransomware Targeting Payment Systems: Financial institutions are increasingly targeted by ransomware attacks aimed at locking them out of payment processing infrastructure and demanding high ransoms.

Conclusion

KYB compliance is essential for financial institutions navigating today’s regulatory landscape. It plays a critical role in verifying business legitimacy, identifying Ultimate Beneficial Owners (UBOs), reducing financial crime risk, and supporting regulatory compliance. By adopting automation, API-driven verification, AI-powered monitoring, and ongoing due diligence practices, businesses can onboard merchants faster, strengthen risk management, and stay audit-ready.

Staying ahead of evolving fraud tactics and regulatory requirements means making KYB a priority. Effective KYB programs combine verification, monitoring, and due diligence to help organizations maintain trust, improve onboarding outcomes, and manage risk throughout the customer lifecycle.

OnBoard by MVSI is an end-to-end merchant onboarding and compliance platform for regulated payments, fintech, and financial services, combining digital onboarding, KYB, AML screening, underwriting, and ongoing due diligence (OCDD) in one system.

Frequently Asked Questions

Why is ongoing KYB monitoring important for fraud prevention?

Fraud is becoming increasingly sophisticated, with threats including synthetic identity fraud, deepfake scams, AI-powered fraud, business impersonation scams, and Fraud-as-a-Service (FaaS) operations. Ongoing KYB monitoring helps financial institutions identify emerging risks, maintain compliance, and detect suspicious activity before it leads to financial loss or regulatory exposure.

What Does KYB Mean in Finance?

KYB (Know Your Business) in finance is a regulatory requirement that ensures financial institutions verify a business’s identity, ownership structure, and legitimacy to prevent fraud and money laundering. Banks and fintech firms use KYB to conduct real-time transaction monitoring, flag suspicious activity, and apply enhanced due diligence for high-risk customers.

What Is KYB in Crypto?

KYB in crypto ensures that businesses using digital assets comply with AML regulations and prevent illicit financial activities. Given the anonymity of blockchain transactions and cross-border nature of crypto, exchanges and payment platforms enforce stricter UBO verification to identify ownership and mitigate fraud risks.