.png)

.webp)

Digital onboarding solutions streamline AML and KYC compliance by automating identity verification, risk assessment, and screening processes, enabling financial institutions to reduce manual effort, improve accuracy, and maintain regulatory compliance efficiently.

Finance is undergoing rapid transformation, driving increased demands for robust Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance. Traditional verification methods—manual checks, paper-based processes, and in-person interactions—are inefficient, costly, and vulnerable to human error. As financial crimes become more complex and regulations more stringent, businesses are turning to digital onboarding solutions to simplify compliance, reduce risks, and improve the customer experience.

In digital onboarding, AML and KYC processes are used to verify customer identities, assess risk, and ensure compliance before and during the customer relationship.

Key Takeaways

- Digital onboarding streamlines AML and KYC compliance by automating identity verification, risk checks, and monitoring processes.

- Automation reduces operational costs and human error by replacing manual document checks and compliance tasks.

- Technologies such as AI and OCR enable real-time compliance, improving accuracy and regulatory alignment.

- Faster onboarding processes improve customer experience while maintaining strong security and verification standards.

Understanding AML and KYC in Digital Onboarding

With the rise of a more connected digital world, AML and KYC measures are crucial for maintaining financial security. These frameworks help institutions guard against financial crimes like money laundering, fraud, and terrorist financing, while also ensuring they stay compliant with global regulations.

Understanding AML Client Onboarding

AML client onboarding is the process financial institutions use to verify a customer’s identity and assess their risk of financial crimes. It involves verifying key details, such as identity documents, conducting background checks, and screening against global watchlists, including those for politically exposed persons (PEPs) and sanctions. The main objectives are to prevent fraud by detecting suspicious activity, manage risk by closely monitoring high-risk clients, and ensure compliance with regulations like the Bank Secrecy Act and the EU AML Directives.

Who Are Politically Exposed Persons (PEPs)?

Politically Exposed Persons (PEPs) are individuals who hold prominent public positions, such as heads of state, senior politicians, judges, military leaders, or executives at state-owned enterprises.

Due to their positions, PEPs are at a higher risk of being involved in financial crimes like bribery and corruption. This also extends to their close family members and associates, who may be involved in illicit activities related to the PEP’s influence. Financial institutions need to carry out enhanced due diligence to monitor these individuals closely and mitigate the risks linked to their political roles. The growing importance of effectively managing PEPs in the fight against financial crime is reflected in recent industry discussions.

Who Are Special Interest Persons (SIPs)?

Special Interest Persons (SIPs) are individuals flagged for their involvement in activities that pose significant risks to financial or reputational integrity. These individuals may be connected to organized crime, terrorism, financial fraud, or other illegal activities.

Unlike PEPs, SIPs are not in political positions but are flagged for their potential role in unethical or criminal behaviour. Financial institutions screen clients against SIP-related databases and apply further checks to comply with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations. Identifying and monitoring SIPs is vital to prevent financial institutions from being unwittingly used for illegal purposes.

Why Are AML and KYC Measures Critical for Financial Institutions?

AML and KYC measures are not just regulatory boxes to tick—they are essential for maintaining an institution's credibility and ensuring its stability. Failing to meet these standards can lead to serious repercussions, including substantial fines, damage to reputation, and even suspension of services.

Here’s why AML and KYC are so crucial:

- Preventing Financial Crime: These measures help institutions identify and block bad actors attempting to exploit the financial system.

- Protecting Reputation: Non-compliance can lead to scandals and erode customer trust, causing long-term damage.

- Avoiding Legal Penalties: Regulators are increasing enforcement, with fines for non-compliance reaching billions each year. Strong compliance helps institutions remain aligned with regulatory requirements.

AML and KYC measures have evolved into highly sophisticated, technology-driven processes. Leveraging advanced digital onboarding solutions enables institutions to navigate these complexities efficiently.

In practice, these AML and KYC processes are typically managed within end-to-end digital onboarding and compliance platforms, where identity verification, screening, and risk assessment are handled as part of a unified workflow rather than separate systems.

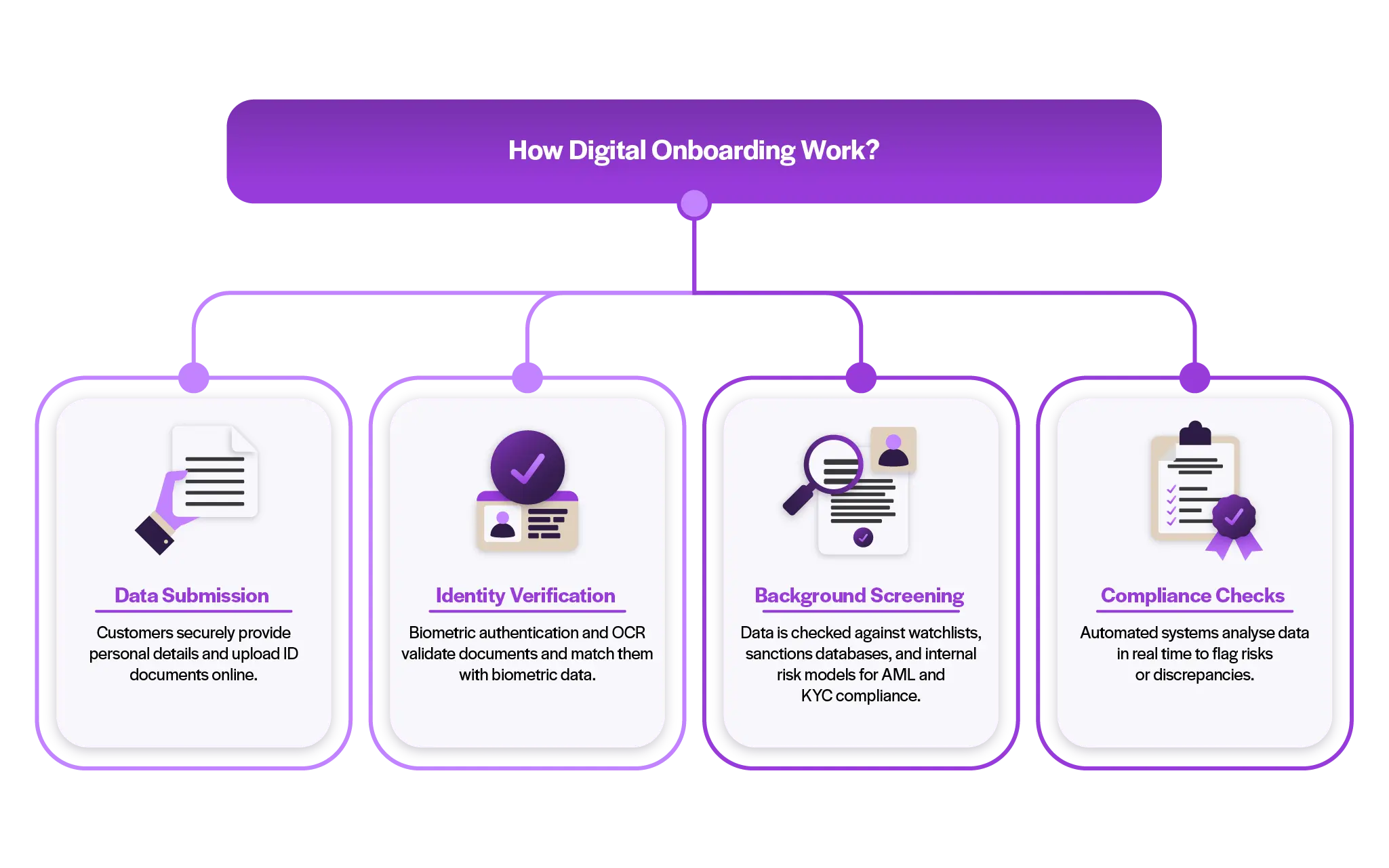

What Is Digital Onboarding, and How Does It Work?

Digital onboarding is the process that enables new customers to join a financial institution through secure online platforms.

By removing the need for in-person meetings and paper forms, it simplifies the customer experience. The process typically involves:

- Data Submission: Customers enter their details and upload identification documents securely online.

- Identity Verification: Technologies like biometric authentication and Optical Character Recognition (OCR) check the validity of documents and match them with biometric data.

- Background Screening: The information is compared with government watchlists, sanctions databases, and internal risk models to ensure compliance with Anti-Money Laundering and Know Your Customer regulations.

- Compliance Checks: Automated systems evaluate the data in real time, flagging any potential risks or discrepancies.

This fully digital solution improves efficiency, reduces delays, and ensures compliance, all while providing a smooth and straightforward experience for customers.

Technologies Powering Digital Onboarding

Digital onboarding relies on cutting-edge technologies to optimize efficiency, security, and compliance:

- Biometric Authentication: Tools like facial recognition, fingerprint scanning, and voice identification ensure accurate identity verification.

- Artificial Intelligence (AI) and Machine Learning (ML): These enable real-time risk assessments, automate manual checks, and detect fraudulent patterns.

- Cloud Platforms: Provide secure, scalable infrastructure for storing sensitive data and ensuring real-time processing.

- Optical Character Recognition (OCR): Digitizes and verifies identity documents quickly and accurately.

The Advantages of Digital Onboarding Solutions

Digital onboarding solutions are transforming how financial institutions approach compliance and customer acquisition. By replacing traditional, paper-heavy processes with efficient, technology-driven workflows, these solutions deliver substantial advantages for both businesses and customers.

Key Benefits of Digital Onboarding

- Cost Reduction via Automation: Automation cuts operational costs by removing the need for manual data entry and reducing paper-based processes. Tasks like document verification and compliance checks, once reliant on human resources, are now streamlined with digital tools, freeing up funds for other strategic priorities.

- Faster, More Efficient Processes: Digital onboarding accelerates the customer journey by automating real-time checks and workflows. What once took days or weeks—such as identity verification and risk assessments—can now be completed in minutes, boosting efficiency and speeding up account activation.

- Improved Accuracy and Compliance: Manual processes come with the risk of human error, potentially leading to compliance issues. Digital solutions use AI-driven identity verification, automated document analysis, and risk scoring to ensure precise, consistent compliance with AML and KYC regulations, reducing fraud and enhancing trust with regulators.

- Better Customer Experience: A smooth onboarding process is key to customer satisfaction and retention. Digital solutions let customers complete the process remotely, using intuitive interfaces on their devices. Features like biometric authentication, real-time updates, and self-service portals create a frictionless experience that fosters trust and loyalty.

Overcoming Challenges in Digital Onboarding

Digital onboarding has transformed compliance processes for AML and KYC, but the path to its full adoption isn’t without obstacles. Financial institutions and businesses face technical, regulatory, and operational challenges in unlocking its full potential.

Key Challenges in Adopting Digital Onboarding

- Technology Integration: One of the major hurdles is integrating digital onboarding systems with existing legacy platforms. This often requires significant investment in infrastructure, time, and expertise. Poor integration can result in inefficiencies, data silos, and disruptions in the customer journey.

- Compliance Management: AML and KYC regulations are constantly evolving and vary by jurisdiction. Digital onboarding solutions must keep up with these changing requirements, necessitating frequent updates and a solid grasp of compliance frameworks.

- Stakeholder Alignment: For digital onboarding to succeed, buy-in is needed from various stakeholders – compliance teams, IT departments, legal advisors, and senior management. Resistance to change or a lack of understanding of the benefits can slow progress or derail the implementation altogether.

Mitigating Risks in Digital Onboarding

While digital onboarding offers unmatched efficiency, it also introduces certain risks that need to be addressed thoughtfully:

- Fraud Prevention: Digital systems are vulnerable to exploitation by fraudsters who may target weaknesses in identity verification processes. To reduce these risks, organizations should implement advanced security measures, such as biometric authentication, liveness detection, and AI-driven fraud detection algorithms.

- Data Breaches: Customer data is a prime target for cybercriminals. To protect sensitive information, strong encryption, multi-factor authentication, and ongoing system monitoring are essential for detecting and responding to threats in real time.

- Technical Glitches: System failures or bugs can disrupt the onboarding process and undermine customer trust. A hybrid approach—blending digital tools with manual oversight—can safeguard against complications in high-risk or complex cases. Regular testing and continuous system improvements are key to preventing disruptions.

By addressing these risks strategically, organizations can maximize the benefits of digital onboarding to streamline AML and KYC compliance, reduce manual errors, and enhance customer satisfaction.

Technological Innovations in AML and KYC Compliance

Recent technological advancements have reshaped AML and KYC compliance, making processes more efficient, accurate, and streamlined. These innovations help financial institutions meet stringent regulations while improving operational efficiency.

Key Technological Advancements

- eKYC (Electronic Know Your Customer)

eKYC replaces traditional paper-based methods with digital workflows, automating identity verification and reducing onboarding time. Real-time checks against AML databases enhance decision-making and support a smoother customer experience. - AI-Driven Identity Verification

AI-powered systems accurately analyze identity documents, biometrics, and data, reducing human error. These tools quickly assess risks and flag potential issues, speeding up the compliance process. - Biometric Authentication

Biometric technologies, such as facial recognition and liveness detection, add an additional layer of security. Real-time verification ensures the person onboarding matches their documents, reducing fraud and boosting security while maintaining fast, efficient onboarding.

Emerging Trends in Compliance Technology

- Machine Learning for Enhanced Risk Detection Machine learning algorithms are transforming fraud detection and compliance. By analyzing patterns in large datasets, these systems can identify suspicious activities and automate complex tasks. They also reduce false positives, a costly and time-consuming issue for financial institutions.

- Blockchain for Transparency and Security Blockchain technology offers a decentralized, immutable ledger that enhances transparency and traceability in financial transactions. Its use in AML and KYC compliance is still developing, but it holds significant potential for secure, efficient identity verification and data sharing.

Practical Applications of Digital Onboarding

Digital onboarding simplifies and accelerates processes that traditionally relied on manual methods, offering efficiency and accuracy. Examples include:

- Online Bank Account Openings: Financial institutions use digital onboarding to enable remote account creation. Automated document verification and biometric authentication ensure KYC and AML compliance while providing a smooth experience.

- Real Estate Transactions: Digital onboarding helps verify identities for tenants, buyers, and sellers, enabling secure background checks and reducing paperwork delays.

- E-Commerce Platforms: Retailers and marketplaces leverage digital onboarding to prevent fraud by verifying identities during account creation.

- Fintech Platforms: Payment apps and digital wallets use eKYC processes to onboard customers quickly, eliminating the need for in-person visits.

How Digital Onboarding Technologies Are Applied Across Industries

Digital onboarding technologies are not limited to financial services but are transforming operations in a variety of sectors:

- Healthcare: Hospitals and telemedicine platforms use digital onboarding to verify patient identities, ensuring secure access to medical records and services.

- Insurance: Providers leverage these solutions to authenticate policyholders and streamline claim processing, reducing fraud risks.

- Sharing Economy: Ride-hailing platforms and short-term rental services employ digital onboarding to verify drivers, hosts, and users, enhancing trust and safety.

- Real Estate: Beyond tenant checks, digital onboarding is used for identity verification in large-scale property transactions, ensuring compliance and reducing administrative burdens.

- E-Commerce: Platforms adopt these tools to streamline registration and payment processes, balancing security with user convenience.

By automating verification and reducing manual errors, digital onboarding is becoming essential for boosting operational efficiency and regulatory compliance across industries. As adoption rises, these solutions are setting a new standard for customer engagement.

Embracing Technology for Smarter Compliance

The rise of digital onboarding solutions is changing how financial institutions manage AML and KYC compliance. By using technologies like AI, biometric authentication, and real-time data analysis, businesses can simplify processes, minimize errors, and improve security. Digital onboarding has moved from being a helpful option to a vital tool for staying competitive in a digital-first world.

The advantages are clear: greater efficiency, cost savings, quicker verification, and a better experience for customers. As regulations continue to change, these solutions help businesses stay compliant while protecting against new risks. Institutions that embrace these technologies not only meet today’s standards but also prepare for future challenges, setting themselves up for long-term success.

This content is provided for general informational purposes only and does not constitute legal or regulatory advice. AML and KYC requirements may vary by jurisdiction and organization.

Frequently Asked Questions

What is the AI solution for KYC?

AI solutions for KYC are used to collect, extract, and verify customer information from identity documents. This enables faster data processing, reduces manual effort, and supports accurate compliance checks.

Can onboarding be done remotely?

Yes, remote onboarding allows customers to upload documents, verify identities using biometrics, and complete compliance checks online, providing a secure and efficient onboarding experience.

What are the risks of digital onboarding?

Risks include fraud, data breaches, and system failures. These can be mitigated through strong encryption, biometric verification, AI-based fraud detection, and regular system updates.

How do digital KYC services ensure fraud prevention?

Digital KYC uses biometrics, AI, and automated checks against sanctions lists, PEPs, and SIPs to detect suspicious activity, verify identities, and support compliance with regulatory requirements.